How the US–Iran Confrontation Is Transmitting an Oil Shock Through Pakistan’s Economy — and Why the Region Cannot Afford to Look Away

The escalating military and diplomatic confrontation between the United States and Iran in early 2026 has triggered a severe energy price shock with structural consequences for Pakistan — one of South Asia’s most economically fragile states. Pakistan’s weekly petroleum import bill has surged 167 percent, from USD 300 million to USD 800 million, as Brent crude crossed USD 112 per barrel and threats to the Strait of Hormuz — conduit for approximately 20 percent of global oil supply — drove freight costs and insurance premiums to historic highs. This paper analyses the mechanisms through which the shock transmits across Pakistan’s macroeconomy: accelerating inflation, current account deterioration, foreign exchange reserve depletion, currency depreciation, and a growing logistics crisis at Karachi port. It critically examines Islamabad’s overland trade corridor strategy and its attendant geopolitical exposure under US secondary sanctions architecture. Drawing on IMF, World Bank, EIA, and Reuters data, it benchmarks Pakistan’s trajectory against the Sri Lanka crisis of 2022 and derives calibrated implications for India’s strategic posture. The central finding is that Pakistan’s crisis reflects structural vulnerability rather than a transient shock — a distinction with significant consequences for regional stability.

I. The Anatomy of a Transmitted Shock

Geopolitical crises rarely confine their consequences to their immediate theatre. The intensifying confrontation between the United States and Iran — a contest over naval access, nuclear capability, and regional influence — has now reached South Asia not as diplomatic turbulence but as domestic emergency. Its primary casualty in the subcontinent is Pakistan.

In April 2026, Prime Minister Shehbaz Sharif confirmed publicly that Pakistan’s weekly petroleum import bill had risen from USD 300 million to USD 800 million — an increase of 167 percent within weeks (Reuters, April 2026). Annualised, the additional burden approaches USD 26 billion, a figure that nearly matches Pakistan’s entire FY2025 merchandise export earnings of USD 29.8 billion (World Bank, 2025). The country is, in effect, generating an import liability equal to its entire export sector — in a single commodity category — during a period of acute reserve stress.

This paper provides a structured, evidence-based analysis of how that shock transmits through Pakistan’s macroeconomic architecture, how Islamabad is responding, and what the crisis portends for South Asia’s strategic landscape.

Pakistan’s incremental annual oil burden now approaches its total export earnings. This is not a price adjustment — it is a stress event of structural proportions, exposing vulnerabilities that predate the current crisis by decades.

II. The Hormuz Variable: Energy Markets Under Geopolitical Strain

The World’s Most Consequential Chokepoint

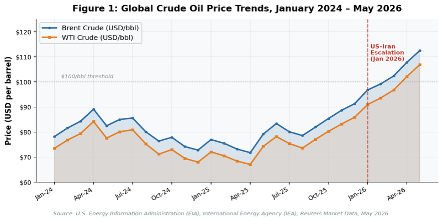

The Strait of Hormuz — the twenty-one-mile-wide passage between Iran and Oman — carries approximately 20 to 21 million barrels of oil per day, representing roughly one-fifth of global oil consumption and nearly 30 percent of all seaborne petroleum trade (EIA, 2024). No viable large-scale alternative exists: Saudi Arabia’s East–West Pipeline handles at most five million barrels per day, and Yemen’s Bab-el-Mandeb strait faces independent interdiction risks from Houthi operations.

The US–Iran confrontation has produced three compounding market effects: a supply shock as Iranian crude exports of approximately 1.5–1.7 mb/d were effectively suspended; a war-risk premium surge across the marine insurance market; and a routing cost inflation as tanker operators divert around the Cape of Good Hope, adding ten to fourteen transit days and an estimated USD 8–12 per barrel in additional freight and fuel costs.

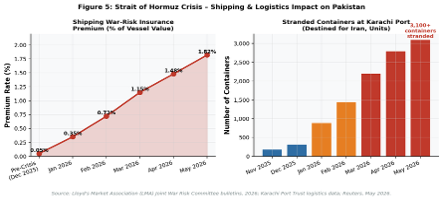

The price outcome is unambiguous. Brent crude averaged USD 78.2 per barrel in January 2024. By May 2026, it had reached USD 112.5 per barrel — a 44 percent increase. War-risk insurance premiums for vessels transiting the Strait rose from 0.05 percent to 1.82 percent of vessel value between December 2025 and May 2026 — a 36-fold increase — adding USD 1.77 million per voyage for a Very Large Crude Carrier (Lloyd’s Market Association, May 2026).

Source: U.S. Energy Information Administration (EIA), Short-Term Energy Outlook, May 2026; IEA Oil Market Report, May 2026; Reuters Market Data, May 2026.

III. Structural Exposure: Why Pakistan Absorbs the Shock Most Acutely

Energy Import Dependence and Fiscal Fragility

Pakistan’s disproportionate exposure to international oil price movements is not incidental — it is architectural. Approximately 85 to 90 percent of the country’s petroleum requirements are met through imports, predominantly from Gulf states whose export logistics depend entirely on unimpeded Hormuz transit (Pakistan Ministry of Petroleum, 2025). Domestic crude production of roughly 69,000 barrels per day satisfies less than 15 percent of national consumption of approximately 500,000 bpd (PBS Economic Survey 2024–25). Unlike India, which has progressively diversified toward discounted Russian crude since 2022, Pakistan possesses no comparable alternative supply option and no functioning strategic petroleum reserve.

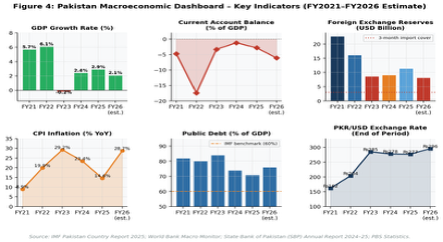

This structural dependence generates what economists term a high pass-through environment: international oil price increases transmit rapidly and comprehensively into domestic fuel prices, transport costs, electricity tariffs, and consumer prices. The IMF estimates Pakistan’s CPI elasticity to oil at 0.4–0.6 percent per 10 percent price increase — among the highest in South Asia. Pakistan’s macroeconomic position entering the crisis was already stressed, as Table 1 and Figure 2 illustrate.

Source: IMF Pakistan Country Report 2025; World Bank Pakistan Macro Poverty Outlook 2025–26; State Bank of Pakistan Annual Report 2024–25; Pakistan Bureau of Statistics Economic Survey 2024–25.

Table 1: Pakistan — Selected Macroeconomic Indicators, FY2022–FY2026 (Estimate)

| Indicator | FY2022 | FY2023 | FY2024 | FY2025 | FY2026 (Est.) |

| GDP Growth Rate (%) | 6.1 | -0.2 | 2.4 | 2.9 | 2.1 |

| CPI Inflation (% YoY) | 19.9 | 29.2 | 23.4 | 14.6 | 28.7* |

| Current Account (% of GDP) | -17.4 | -3.3 | -1.2 | -2.8 | -6.1* |

| Foreign Exchange Reserves (USD Bn) | 16.2 | 8.7 | 9.1 | 11.4 | 8.2* |

| Public Debt (% of GDP) | 80 | 84 | 74 | 71 | 76* |

| PKR / USD Exchange Rate | 204 | 285 | 278 | 277 | 296* |

| Annual Oil Import Bill (USD Bn) | 16.8 | 17.3 | 15.6 | 18.2 | 28.9* |

IV. Transmission Mechanisms: From Oil Price to Economic Stress

The Import Bill Surge

The most immediately quantifiable effect is the import bill shock. Pakistan’s annualised petroleum import expenditure is projected to reach USD 28.9 billion in FY2026, compared to USD 18.2 billion in FY2025 — an increase of USD 10.7 billion (IMF, 2025; Ministry of Finance, 2026). Three compounding factors drive this: the 44 percent rise in crude prices; the necessity of spot-market procurement as contracted Gulf supply was disrupted, attracting premium pricing; and the freight cost elevation of USD 8–12 per barrel above spot prices due to tanker rerouting and war-risk surcharges.

Source: Pakistan Ministry of Finance; IMF Pakistan Country Report 2025; PM Shehbaz Sharif statement reported by Reuters, April 2026; State Bank of Pakistan import data.

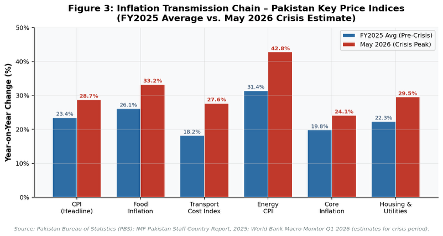

Inflation and Currency Dynamics

The inflationary transmission operates through multiple channels simultaneously. Retail fuel prices rise directly; diesel cost increases — estimated at 25–30 percent — propagate through Pakistan’s fragmented supply chains as elevated transport costs, which in turn drive food commodity prices upward by an estimated 15–20 percent. Electricity tariffs face additional pressure from higher fuel-oil generation costs. Pakistan Bureau of Statistics data shows food and beverages constitute 35–40 percent of the CPI basket for lower-income households — making inflation here both pervasive and regressive.

Headline CPI, which had eased to 14.6 percent by mid-FY2025 under the IMF programme, is tracking toward 28–30 percent. Energy CPI is estimated to have surged 42.8 percent year-on-year by May 2026. Critically, IMF Extended Fund Facility conditionalities prohibit broad-based energy subsidies, forcing the full price pass-through onto consumers. The rupee has depreciated from PKR 277 per dollar at end-FY2025 to approximately PKR 296 — a 6.8 percent decline that further inflates the domestic cost of dollar-denominated imports.

Source: Pakistan Bureau of Statistics (PBS) CPI Report, May 2026; IMF Pakistan Staff Country Report 2025; World Bank Pakistan Macro Monitor Q1 2026; SBP Monetary Policy Statement, April 2026.

Table 2: Pakistan External Sector Stress Indicators, FY2024–May 2026

| Indicator | FY2024 | FY2025 | Q1 FY2026 | May 2026 (Est.) |

| Oil Import Bill (USD Bn, Quarterly) | 3.9 | 4.6 | 5.9 | 9.6 |

| Trade Deficit (USD Bn, Quarterly) | -5.8 | -6.2 | -8.1 | -12.4 |

| Current Account Balance (USD Bn, Quarterly) | -0.3 | -0.7 | -2.1 | -4.6 |

| Foreign Exchange Reserves (USD Bn) | 9.1 | 11.4 | 9.8 | 8.2 |

| PKR / USD (End of Period) | 278 | 277 | 285 | 296 |

| Import Cover (Months of Reserves) | 2.1 | 2.5 | 2.1 | 1.9 |

V. The Logistics Dimension: Karachi Port and the Supply Chain Rupture

The energy shock has been accompanied by a broader logistics crisis that compounds the macroeconomic stress. More than 3,100 shipping containers destined for Iranian buyers lie stranded at Karachi port — unable to proceed due to shipping line restrictions, US Treasury OFAC alerts to maritime intermediaries, and marine insurance refusals (Karachi Port Trust, May 2026; Reuters, May 2026). The backlog represents an estimated USD 280–350 million in cargo value and is generating downstream congestion that is delaying commercial shipments unrelated to Iran.

Bulk cargo rates on the Arabian Gulf–Karachi corridor have tripled: from USD 20–22 per metric tonne in FY2025 to USD 62–70 per metric tonne by May 2026. Container rates for a standard twenty-foot unit on the same route have risen from USD 850 to USD 2,400 — a 182 percent increase (Baltic Exchange, May 2026). The cumulative effect is a supply chain under severe strain, with consequences extending beyond petroleum into food imports, industrial raw materials, and pharmaceutical supply chains.

Source: Lloyd’s Market Association (LMA) Joint War Risk Committee Premium Bulletins, May 2026; Karachi Port Trust Logistics Report, May 2026; Reuters, “Pakistan port backlog deepens,” May 2026.

Table 3: Pakistan–Gulf Trade Logistics — Pre-Crisis vs. Post-Crisis Comparison

| Metric | Pre-Crisis (Dec 2025) | Post-Crisis (May 2026) | Change |

| Gulf–Karachi Bulk Freight (USD / MT) | $20–22 | $62–70 | +210% |

| Container Rate (20 ft, Gulf–Karachi) | $850 | $2,400 | +182% |

| War-Risk Insurance Premium (% vessel value) | 0.05% | 1.82% | +3,540 bps |

| Average Transit Time (days) | 6–8 | 15–20 | +133% |

| Delivered Oil Cost Premium (USD / bbl) | — | ~$10–12 | Added cost |

| Stranded Containers at Karachi | ~0 | 3,100+ | New phenomenon |

VI. Islamabad’s Response: Economic Pragmatism and Geopolitical Exposure

The Overland Corridor Initiative

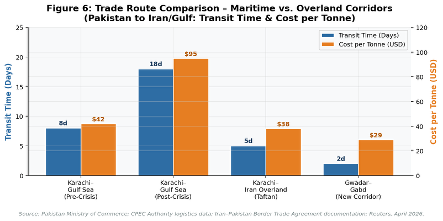

Confronted with maritime disruption on a scale that threatened supply chain viability, Islamabad activated six overland trade corridors connecting Karachi, Port Qasim, and Gwadar to Iranian border crossings at Taftan and Gabd. The most operationally significant is the Gwadar–Gabd route — constructed under China-Pakistan Economic Corridor infrastructure — which reduces transit time from approximately eighteen hours to three to four hours and lowers transport costs by an estimated 40 percent relative to pre-crisis sea freight rates (CPEC Authority, 2026).

Source: Pakistan Ministry of Commerce; CPEC Authority Logistics Report 2025–26; Iran–Pakistan Border Trade Commission statement, April 2026; Reuters, April 2026.

Table 4: Pakistan–Iran Trade Route Options — Comparative Assessment

| Route | Mode | Transit Time | Cost (USD/tonne) | Sanctions Risk |

| Karachi–Gulf (Maritime, Pre-Crisis) | Sea | 6–8 days | $20–42 | None |

| Karachi–Gulf (Maritime, Post-Crisis) | Sea | 15–20 days | $62–95 | Very High |

| Karachi–Taftan Border (Road) | Overland | 24–30 hrs | $38 | OFAC Exposure |

| Gwadar–Gabd Corridor (CPEC) | Overland | 3–4 hrs | $29 | OFAC Exposure |

The Geopolitical Contradiction

The economic rationale for the overland corridors is clear. Their geopolitical implications are considerably more complex. Washington’s strategic objective is the comprehensive economic isolation of Iran — a policy designed to compel concessions on nuclear enrichment, ballistic missile development, and proxy network operations. Overland corridors enabling third-country goods to enter Iran by land directly erode the maritime dimension of that strategy, creating a vulnerability that US sanctions architects are well-positioned to address through secondary sanctions.

Pakistan’s exposure is acute. Its banking sector — dependent on US dollar correspondent relationships for international trade settlement — is particularly vulnerable to OFAC designation or warning letters. A loss of correspondent banking access would be functionally catastrophic for Pakistan’s external trade. The situation is further complicated by Islamabad’s concurrent diplomatic positioning: Pakistan hosted the first round of US–Iran talks in April 2026, presenting itself as a neutral mediator. The simultaneous operation of trade facilitation corridors into Iran is structurally inconsistent with credible neutrality, and Washington has noted the contradiction.

Islamabad faces a strategic dilemma with no clean resolution: economic necessity demands the corridors remain open, while geopolitical survival requires that Washington does not conclude Pakistan is systematically facilitating sanctions evasion. Both imperatives are real. They are also in direct tension.

VII. Benchmarking the Crisis: Parallels with Sri Lanka, 2022

The 2022 Sri Lankan economic crisis — culminating in sovereign default, acute fuel shortages, and the collapse of civilian governance — remains the most instructive regional precedent. The structural parallels with Pakistan’s current situation are notable: foreign exchange reserve depletion, an energy import shortfall, accelerating inflation, and mounting political pressure on governing institutions. Table 5 provides a comparative assessment.

| Indicator | Sri Lanka (2022 Peak) | Pakistan (May 2026) |

| Foreign Exchange Reserves (USD Bn) | 1.6 | 8.2 |

| Peak CPI Inflation (% YoY) | 69.8% | 28.7% (rising) |

| External Debt / GDP | ~120% | ~42% |

| IMF Programme Status | USD 2.9 Bn (negotiating) | USD 7 Bn (active EFF) |

| Fuel Supply Situation | Severe shortage; 12+ hr queues | Elevated costs; load-shedding |

| Political Stability Outcome | President fled; government collapsed | Stress elevated; no collapse yet |

| Sovereign Default Status | Defaulted April 2022 | Risk elevated; not imminent |

| Affected Population | 22 million | 240 million |

Pakistan diverges from Sri Lanka in three materially significant respects: its external debt-to-GDP ratio is far lower; it maintains an active IMF programme with ongoing disbursements; and its geopolitical significance — as a nuclear-armed state bordering Afghanistan, India, Iran, and China — generates external support that Colombo could not access. These are meaningful buffers. They are not, however, structural cures.

VIII. Regional Dimensions: India, China, and the Broader Strategic Landscape

India’s Strategic Position

India is not insulated from the global oil price shock. Its petroleum import bill has risen substantially. Yet the comparison with Pakistan’s vulnerability is, at present, one of kind rather than degree. India maintains foreign exchange reserves exceeding USD 640 billion (Reserve Bank of India, April 2026), has diversified its crude sourcing — with Russian Urals accounting for approximately 40 percent of imports — and possesses a GDP roughly twelve times Pakistan’s in nominal terms. These advantages are strategic as much as economic: they provide the policy space to absorb exogenous shocks without existential consequences.

For New Delhi, Pakistan’s crisis generates two distinct categories of strategic concern. The first is security: economic distress in Pakistan correlates historically with political volatility, institutional stress within the military establishment, and a more permissive environment for non-state actors. A nuclear-armed state undergoing acute economic deterioration is a qualitatively different risk profile than a stable adversary. The second is alignment: Pakistan’s economic desperation accelerates its dependence on Chinese financing — through CPEC credit lines, bilateral currency swap arrangements, and emergency commodity credits — deepening Sino-Pakistani strategic integration at a moment when India-China tensions remain elevated.

China’s Strategic Stake

Beijing has both an economic and a strategic interest in the unfolding situation. CPEC — a USD 65-plus billion infrastructure commitment — makes China the principal stakeholder in Pakistan’s economic stability. Chinese port operators at Gwadar are de facto participants in the overland corridor initiative. China also maintains an independent interest in Iranian energy access; China-Iran bilateral trade, estimated at USD 35–40 billion annually, includes significant crude oil imports that Beijing routes through arrangements that circumvent US sanctions. The alignment of Chinese and Pakistani interests in maintaining Iranian commercial connectivity — while Washington seeks to sever it — creates a structural tension with implications for the broader regional order.

IX. Conclusion: Structural Vulnerability and the Limits of Crisis Management

The US–Iran confrontation did not create Pakistan’s economic vulnerabilities. It exposed them. Decades of energy import dependence, chronic fiscal imbalances, an underdeveloped export base, and a pattern of crisis-followed-by-bailout-followed-by-return-to-vulnerability have produced an economy structurally incapable of absorbing even moderate external shocks without systemic stress. The current crisis is the expression of that architecture under pressure.

Islamabad’s short-term options are constrained on multiple dimensions simultaneously. It cannot afford to fully pass through oil costs — the social consequences would be politically destabilising. It cannot afford to subsidise them — the IMF programme would be at risk. It cannot close the overland corridors — economic necessity is too acute. It cannot fully open them — Washington’s patience with sanctions circumvention has limits. The result is a policy environment defined by improvisation rather than strategy.

For the broader region, the crisis carries a lesson that extends beyond Pakistan’s borders. In an era of weaponised interdependence — where geopolitical confrontations in one region transmit as economic emergencies in another — structural resilience is not a macroeconomic luxury. It is a precondition for an independent policy agency. India’s relative insulation from the current shock reflects not fortune but deliberate choices made over years: reserve accumulation, supply diversification, export development. Pakistan’s exposure reflects the opposite.

The question for Pakistan is not whether it can survive this crisis — with sufficient external support, it likely can. The question is whether it will emerge from it any less structurally exposed than before. On the evidence of 24 IMF programmes across six decades, the answer will depend not on the resolution of the current emergency, but on whether its conclusion is followed by genuine structural reform or by the familiar return to deferred choices.