Russia’s war in Ukraine has transformed North Korea from China’s dependent buffer into a more autonomous strategic actor—weakening Beijing’s exclusive leverage and generating cascading security dilemmas across Northeast Asia.

INTRODUCTION

When Xi Jinping arrived in Pyongyang on 8 June 2026—his first overseas trip of the year—Kim Yo Jong had already framed the strategic terms. Two days before Xi landed, she declared North Korea’s nuclear status an “irreversible and final conclusion.” Five days before his arrival, Kim Jong Un inspected the country’s third publicly disclosed uranium enrichment facility and pledged exponential expansion of his nuclear forces (KCNA, 3 June 2026). The choreography of Xi’s welcome was impeccable. Its strategic meaning was not.

This article addresses a precise puzzle: why is Xi investing maximum diplomatic capital in North Korea at the moment when China’s exclusive leverage over Pyongyang has demonstrably eroded? The answer lies in Russia. Moscow’s February 2022 invasion of Ukraine created conditions North Korea was uniquely positioned to exploit—a wartime arms market worth over $10 billion, advanced military technologies China had historically withheld, and a credible outside option that ended Beijing’s near-monopoly over Pyongyang. The result is a North Korea that is more autonomous, more capable, and more nuclear than at any point in its history—a challenge that now confronts China as much as it does the United States.

CHINA’S HISTORICAL LEVERAGE

China’s leverage over North Korea rested on three pillars: buffer-state logic, economic dominance, and diplomatic protection. The Korean War (1950–1953) established North Korea as indispensable to China’s northeastern security perimeter. For seven subsequent decades, Beijing supplied over 90 percent of Pyongyang’s fuel, accounted for more than 95 percent of its trade, and wielded its UN Security Council veto to shield North Korea from crippling sanctions. The operating assumption was that economic dependency would translate into political compliance. Russia’s war exposed that assumption as structurally flawed.

RUSSIA’S WAR AND NORTH KOREA’S STRATEGIC REVIVAL

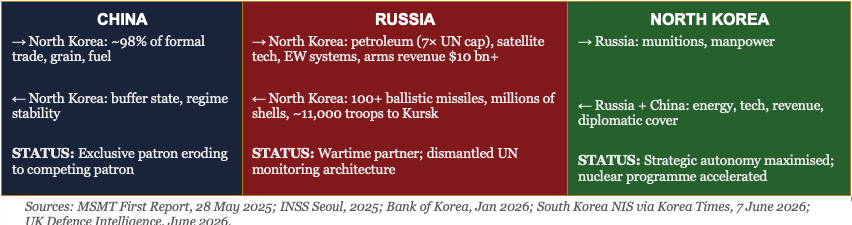

The transformation began in September 2023 when Kim Jong Un travelled to Russia’s Vostochny Cosmodrome. What followed was documented systematically by the Multilateral Sanctions Monitoring Team (MSMT), established after Russia vetoed the UN Panel of Experts in March 2024. The MSMT’s first report (28 May 2025) confirmed that North Korea transferred at least 100 KN-23 ballistic missiles to Russia between January and December 2024 alone—subsequently launched against Ukrainian cities—alongside millions of artillery rounds.

The returns Pyongyang received reordered its strategic position. The Seoul-based INSS estimated North Korean munitions revenue at over $10 billion between mid-2023 and end-2025—approximately one-third of its nominal GDP. The Bank of Korea confirmed 3.7 percent GDP growth in 2024, the fastest in eight years, driven by a 10.7 percent surge in heavy industry. South Korea’s National Intelligence Service (NIS) assessed that 2025 petroleum imports from China and Russia together exceeded the UN Security Council’s 500,000-barrel annual cap by approximately seven times (Korea Times, 7 June 2026).

Technology transfers proved more consequential than cash. US Forces Korea Commander General Xavier Brunson told the Senate Armed Services Committee in April 2025 that Russia was “expanding sharing of space, nuclear, and missile-applicable technology, expertise, and materials” and that this “will enable advancements of DPRK’s weapons of mass destruction programme across the next three to five years.” North Korea’s first successful reconnaissance satellite launch in November 2023—following two earlier failures—came after Russian technical assistance. Each of these transfers addressed precisely the capabilities China had strategically withheld to preserve leverage.

Table 1: North Korea Before and After Russia’s War (2022–2026)

| Dimension | Before 2022 | After 2022 | Strategic Effect |

| External Patron(s) | China sole patron; near-total dependency | China + Russia dual-patron equilibrium | Pyongyang plays each against the other |

| Energy Supply | China ~90% of fuel; UN petroleum cap broadly respected | Russia delivers petroleum ~7× UN cap in 2025 (South Korea NIS) | Energy sanctions effectively nullified |

| Arms Revenue | Negligible; sanctions-constrained exports | ~$10 bn+ from munitions to Russia, 2023–2025 (INSS Seoul) | ~1/3 of nominal GDP; fastest GDP growth in 8 years |

| Military Technology | Largely indigenous; no patron transferred advanced systems | Russia: satellite tech, EW systems, missile performance data (MSMT, May 2025) | Capabilities China withheld now acquired via Moscow |

| Diplomatic Shield | China veto alone; UN Panel of Experts operational since 2010 | Russia vetoed PoE renewal March 2024; dual UNSC cover | Monitoring architecture dismantled; sanctions enforcement collapsed |

| Nuclear Programme | ‘Denuclearisation’ in every Xi–Kim joint readout 2018–2019 | China dropped ‘denuclearisation’ from Nov 2025 arms-control white paper | China’s core policy demand abandoned as unenforceable |

| Strategic Autonomy | Severely constrained — one patron, one lifeline | Substantially enhanced — credible outside option operational | China’s coercive monopoly eliminated |

Sources: MSMT First Report, 28 May 2025; INSS Seoul, 2025; Bank of Korea, Jan 2026; NIS via Korea Times, 7 June 2026; Foreign Policy, 9 Jan 2026; SIPRI Yearbook 2026.

XI’S DILEMMA: CHINA’S INFLUENCE BECOMES LESS EXCLUSIVE

China still accounts for approximately 98 percent of North Korea’s formal trade, which recovered to $2.73 billion in 2025 (Bank of Korea, January 2026). But leverage is not the same as dependency. Leverage is the capacity to compel behavioural change through credible threat of support withdrawal—and that capacity depends on what happens to North Korea if China actually applies pressure.

Before 2022, the answer was severe economic disruption with no viable alternative. After 2022, North Korea has a Russian partner supplying fuel at seven times the UN-sanctioned cap, generating arms revenue in off-book form, extending diplomatic protection that reduces the cost of Chinese pressure to manageable levels, and transferring technologies China had consciously withheld. An outside option does not need to replace China to be decisive; it merely needs to be credible enough that Beijing cannot threaten disruption without risking strategic loss.

The most revealing indicator is linguistic. China’s official position had for decades centred on “denuclearisation of the Korean Peninsula,” appearing in defence white papers and UN diplomacy as proof of Chinese opposition to Pyongyang’s nuclear programme. In November 2025, Beijing’s latest arms-control white paper dropped that phrase entirely, substituting vague calls for “peace” and “political means” (Foreign Policy, 9 January 2026). During Xi’s June 2026 Pyongyang visit, Al Jazeera noted the “conspicuous absence of denuclearisation from the agenda.” A patron that cannot name its core policy objective without risking loss of the client relationship has not retained that objective as an operational lever.

Three structural mechanisms explain the erosion. First, Russia eliminated China’s monopoly rent by providing a credible alternative patron. Second, by vetoing the UN Panel of Experts’ renewal in March 2024, Russia dismantled the institutional monitoring architecture through which Beijing had maintained collective pressure for fourteen years. Third, Moscow transferred precisely the capabilities—satellite expertise, missile performance data, electronic warfare systems—that Beijing had withheld as its primary source of coercive advantage. China never shared these technologies because withholding them was the point. Russia had no such incentive.

Table 2: China vs Russia — Sources of Influence Over North Korea

| Type of Influence | China | Russia | Relative Strategic Value |

| Trade & formal commerce | ~98% of formal trade ($2.73 bn, 2025) | Minimal formal trade | China dominant — but mutual dependency limits coercive use |

| Energy supply | Fuel supply (nominally cap-compliant on paper) | Petroleum at 7× UN annual cap (2025 NIS) | Russia decisive for sanctions-busting energy |

| Arms revenue | None | $10 bn+ in munitions payments, 2023–2025 | Russia created North Korea’s largest income source in history |

| Military technology | Withheld advanced systems to preserve leverage | Satellite tech, EW, air-defence, ICBM data (MSMT, May 2025) | Russia transferred exactly what China refused to share |

| Diplomatic cover | UNSC veto (primary shield 1950–2022) | Vetoed PoE renewal March 2024; co-blocking all resolutions | Russia now co-equal diplomatic shield |

| Nuclear deterrence signal | No explicit endorsement of DPRK nuclear status | Implicit endorsement via technology transfers | Russia normalising DPRK nuclear status Beijing cannot reverse |

| Troop/combat experience | None | ~11,000 troops deployed to Kursk (NIS, Feb 2026) | Combat exposure China cannot replicate diplomatically |

Sources: MSMT First Report, May 2025; Bank of Korea, Jan 2026; South Korea NIS, 2026; UK Defence Intelligence, 2026.

Figure 1: China–Russia–North Korea Strategic Triangle (2022–2026)

COMPARATIVE ASSESSMENT: BEFORE AND AFTER UKRAINE

The structural shift since 2022 is categorical, not merely incremental. Before the Ukraine war, North Korea operated under a single-patron model: economic survival required Chinese acquiescence, and Beijing’s coercive capacity was near-total. After 2022, North Korea operates within a triangular equilibrium—playing Beijing and Moscow against each other with strategic sophistication. China’s position has shifted from exclusive patron to competing patron, a fundamentally different relationship even if trade volumes remain high.

The nuclear dimension sharpens this transformation. The SIPRI Yearbook 2026, released the morning Xi arrived in Pyongyang, estimates North Korea at approximately 60 warheads as of January 2026, with fissile material for at least 30 more. Kim’s June 3 inspection of a third publicly disclosed enrichment site signals further acceleration. This expansion proceeded without Chinese approval and despite Chinese preferences—evidence that Beijing’s nuclear leverage is now effectively inoperative.

Table 2: Global Nuclear Warhead Inventories — January 2026

| State | Total Warheads | Deployed | Programme Trajectory (2025–26) |

| Russia | ~5,459 | ~4,380 | New START expired Feb 2026; Sarmat ICBM tests failed again; Oreshnik IRBM deployed to Belarus |

| United States | ~5,177 | ~3,700 | Sentinel ICBM + Columbia SSBN in production; B61-13 gravity bomb first unit completed 2025 |

| China | ~620 | ~24 | Fastest expansion globally; ~100 new warheads/yr since 2023; 775+ missile silos by Jan 2026 |

| North Korea | ~60 | N/A | 4 enrichment sites running continuously; capacity doubled in 5 yrs; 3rd site unveiled 3 June 2026 |

| India | ~190 | N/A | Expanded to ~190 by early 2026; long-range systems targeting China prioritised |

| Pakistan | ~170 | N/A | Steady expansion; new fissile material production ongoing |

| United Kingdom | ~225 | ~120 | Ceiling raised toward 260 per 2021 Integrated Review |

| France | ~290 | ~280 | Stable; ASMP-A modernisation ongoing |

| Israel | ~90 | N/A | Modernising; Negev Research Center construction intensified 2025 |

Sources: SIPRI Yearbook 2026, Chapter 8, H.M. Kristensen and M. Korda, released 8 June 2026 (sipri.org); Federation of American Scientists, ‘Status of World Nuclear Forces, 2026,’ Kristensen, Korda, Johns, Knight-Boyle (fas.org). New START expired February 2026; US/Russia deployed figures no longer verifiable by treaty mechanism. All figures are estimates.

CONCLUSION

Xi’s Pyongyang visit produced pledges of economic cooperation and no mention of denuclearisation. Kim called Xi “the greatest state guest” and characterised China’s choice of North Korea as Xi’s first foreign destination of 2026 as “the most encouraging support.” Beijing received the imagery it wanted. Pyongyang yielded nothing of strategic substance.

Russia’s war was never intended to reshape the balance of power on the Korean Peninsula. Yet by generating over $10 billion in North Korean arms revenue, transferring critical military technologies, and dismantling the UN monitoring architecture, it has eroded Beijing’s exclusive leverage over its most important buffer state. China’s dilemma is not that North Korea is hostile—it is that North Korea is now strategically autonomous. The result is a more volatile Northeast Asia and an Indo-Pacific in which China must contend with an unconstrained nuclear neighbour it can neither manage nor ignore.

Xi’s dilemma is not that North Korea is hostile—it is that North Korea is now strategically autonomous. That is a harder problem for Beijing, and a more volatile one for the Indo-Pacific.

PRINCIPAL SOURCES

1. SIPRI Yearbook 2026, Chapter 8 (‘World Nuclear Forces’), H.M. Kristensen and M. Korda. Stockholm International Peace Research Institute, released 8 June 2026. sipri.org

2. Federation of American Scientists. ‘Status of World Nuclear Forces, 2026.’ Kristensen, Korda, Johns, Knight-Boyle. fas.org/initiative/status-world-nuclear-forces

3. Multilateral Sanctions Monitoring Team (MSMT). MSMT/2025/1, ‘Unlawful Military Cooperation including Arms Transfers between North Korea and Russia.’ 28 May 2025. msmt.info

4. US Forces Korea. Testimony of General Xavier Brunson before the US Senate Armed Services Committee. April 2025.

5. Congressional Research Service. ‘Russia–North Korea Relations.’ CRS Report IF12760. Updated 2025.

6. Institute for National Security Strategy (INSS Seoul). North Korea Economic and Military Assessment 2025.

7. Bank of Korea. GDP estimates for North Korea, 2024 (August 2025) and bilateral trade data (January 2026).

8. South Korea NIS assessments via Yonhap and Korea Times, 2025–2026.

9. UK Defence Intelligence. North Korean casualties in Kursk Oblast. January and June 2026.

10. RUSI. ‘Russia Is Now Actively Funding North Korea’s Nuclear Programme.’ July 2025.

11. Foreign Policy. ‘China’s Quiet Retreat From North Korean Denuclearization.’ 9 January 2026.

12. Al Jazeera. ‘China’s Xi, North Korea’s Kim Pledge to Boost Ties at Rare Pyongyang Summit.’ 9 June 2026.

13. KCNA. Kim Jong Un address at new uranium enrichment facility. 3 June 2026.

14. Korea Times. ‘N. Korea Exports 1.5 Million Tons of Coal in 2025 Despite Sanctions.’ 7 June 2026.