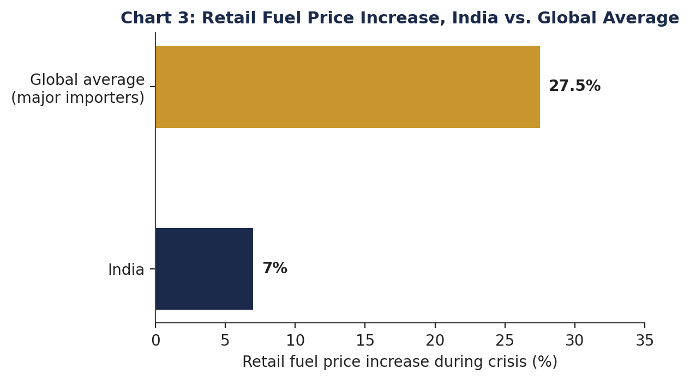

When Iranian forces effectively closed the Strait of Hormuz on 28 February 2026, global oil markets braced for catastrophe. Roughly one-fifth of the world’s seaborne oil and a comparable share of liquefied natural gas pass through this narrow channel (Congressional Research Service 2026; U.S. Energy Information Administration 2024). India, importing close to 90 percent of its crude oil and 60 percent of its liquefied petroleum gas—with nearly half of that crude historically transiting Hormuz (Atlantic Council 2026)—appeared uniquely exposed. Analysts anticipated rationing and empty cylinders. Yet across four months of closure, Indian petrol stations stayed open, LPG deliveries continued, and retail prices rose by roughly seven percent against a global average closer to twenty-five to thirty percent (Ministry of Petroleum and Natural Gas 2026). Why did one of the world’s most import-dependent economies escape what so many others could not? The answer lies less in fortune than in a decade of institutional preparation.

The Paradox of Vulnerability

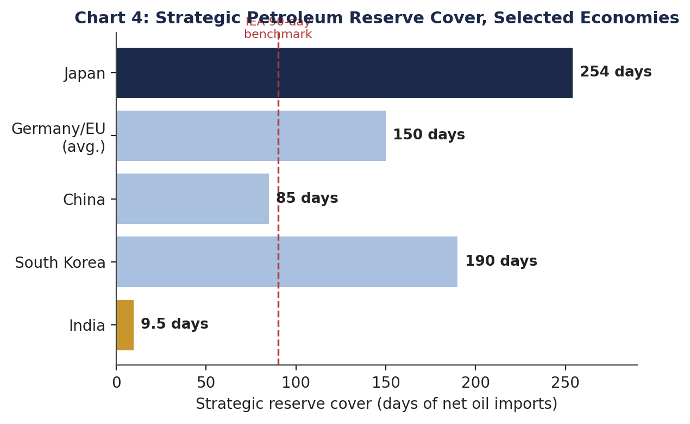

On paper, India looked more fragile than Japan, South Korea, Germany, or China. Japan imports nearly all its crude oil yet holds reserves equivalent to roughly 254 days of net imports across government and industry stockpiles (Al Jazeera 2026; U.S. Energy Information Administration 2026). South Korea’s reserves cover close to 180–208 days (Statista 2026). China’s combined strategic and commercial inventories approach eighty to ninety days of consumption (WION 2026). India’s strategic petroleum reserve, by contrast, stood at 5.33 million tonnes—barely nine to ten days of cover—well short of the International Energy Agency’s ninety-day benchmark, a standard from which India, as a non-member, is in any case exempt. India’s Hormuz exposure was also steeper: roughly 45 percent of crude, half its LNG, and as much as 90 percent of its LPG imports traversed the strait before the crisis (Atlantic Council 2026). By the conventional metrics of stockpiles and chokepoint dependence, India was the more exposed economy, not the less.

Table 1. Comparative Energy Dependence of Major Oil-Importing Economies

| Country | Oil Import Dependence | Hormuz Exposure (pre-crisis) | Strategic Reserve Cover | Primary Government Response |

| India | ~88–90% | ~45% crude; ~50% LNG; ~90% LPG | ~9.5 days (5.33 MMT) | Supply diversification, refinery reconfiguration, price absorption; no rationing |

| Japan | ~99% | High (Gulf-dependent crude basket) | ~254 days | Coordinated IEA stockpile release |

| South Korea | ~93%+ | High (Middle East share of crude) | ~180–208 days | Retail price caps; coordinated reserve release |

| Germany | Moderate–high | Lower direct exposure (diversified European supply) | ~100–200 days (EU avg.) | Fuel tax cuts |

| China | ~72% | Partial (some tanker access retained) | ~80–90 days | Drew on large state and commercial stockpiles |

Sources: Atlantic Council (2026); U.S. Energy Information Administration (2026); Al Jazeera (2026); Statista, IEA data (2026); WION (2026); Ministry of Petroleum and Natural Gas, Government of India (2026).

Preparedness Before the Crisis

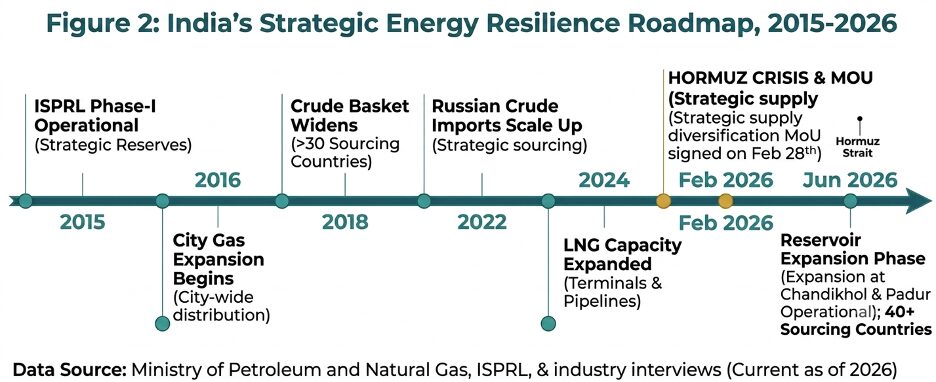

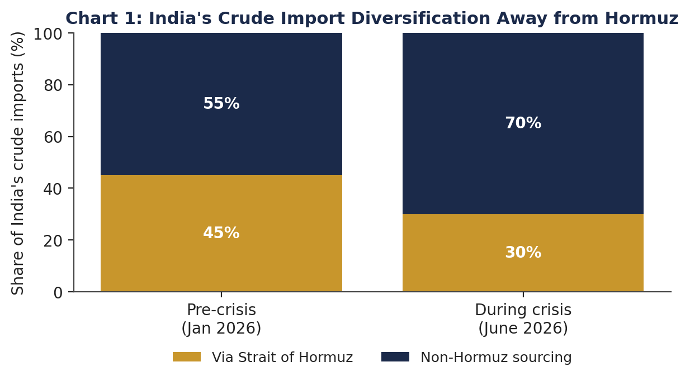

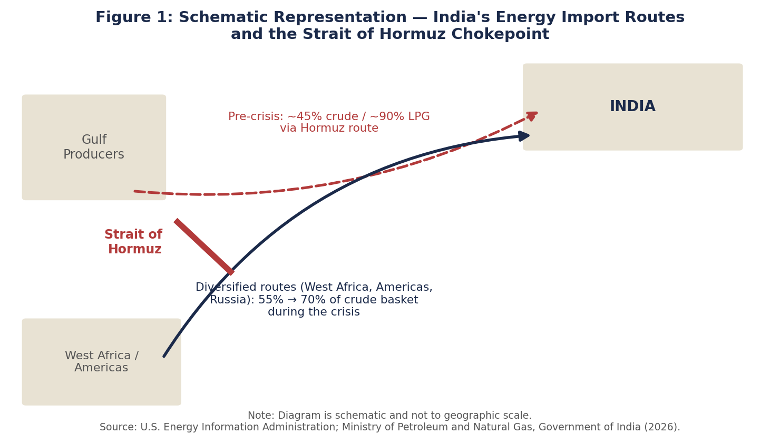

The resilience that followed was not improvised. Over the preceding decade, India quietly rebuilt the architecture of its energy supply chain. Crude sourcing diversified from roughly twenty-seven countries a decade ago to more than forty by 2026, as refiners invested in the flexibility to process varied crude grades—built through incremental upgrades rather than overnight retrofits (B. Ashok, former Chairman, Indian Oil Corporation, interview, 2026). When the crisis struck, non-Hormuz sourcing rose from 55 to 70 percent within weeks, drawing on West Africa, the Americas, and Russia (Ministry of Petroleum and Natural Gas, interview, 2026). This shift was possible only because relationships, quality assurance, and port logistics for these alternative grades had already been established.

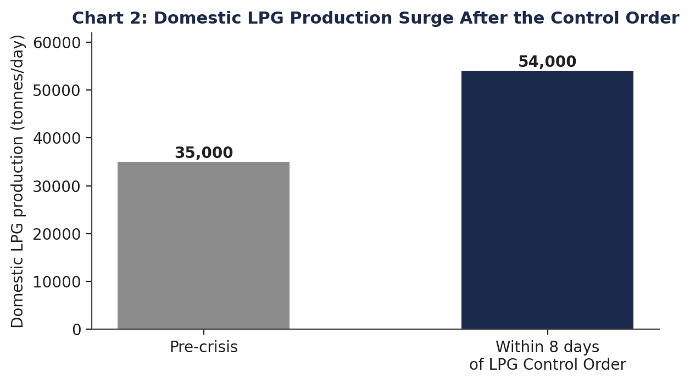

Refining flexibility proved equally decisive. Within eight days of the strait’s closure, the government invoked the Essential Commodities Act to issue an LPG Control Order, directing refiners to adjust their product slate. Domestic LPG output rose from roughly 35,000 to 54,000 tonnes a day within a week, substituting for lost Gulf cargoes (Ministry of Petroleum and Natural Gas, interview, 2026)—achievable only because India already possessed sufficient indigenous refining capacity. Expanding city gas distribution, now covering close to three hundred cities, enabled demand-side substitution toward piped natural gas. India’s digital public infrastructure, including OTP verification for cylinder delivery, prevented diversion into grey markets even as households worried about shortages. None of these levers could have been built during the crisis itself; they were the product of a decade-long investment cycle.

Comparative Crisis Management

Elsewhere, governments leaned on blunter instruments. IEA members coordinated the release of 400 million barrels from emergency stockpiles in March 2026 to calm markets (Statista 2026). South Korea capped retail fuel prices. Germany cut fuel taxes, the United Kingdom largely allowed international price movements to pass through, and Spain released some 11.5 million barrels of reserves over ninety days (Al Jazeera 2026). Several Asian economies turned to demand suppression—shortened work weeks, restricted driving, early pump closures. India pursued a different sequence. Rather than rationing supply broadly, it absorbed cost through fiscal measures: an excise duty cut of roughly ₹10 per litre on petrol and diesel, forgoing about ₹1.7 lakh crore in revenue, while oil marketing companies absorbed daily under-recoveries that peaked near ₹1,000 crore (Ministry of Petroleum and Natural Gas, interview, 2026). Demand management was targeted narrowly at commercial and bulk LPG users, shielding households first.

Energy Security Beyond Oil

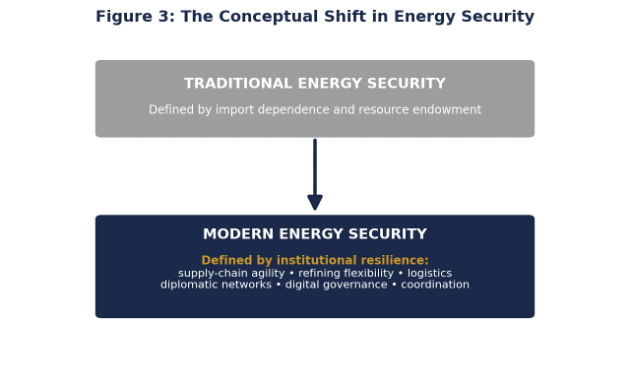

The Hormuz episode suggests that the traditional metrics of energy security—import dependence and reserve volumes—capture only part of the picture. India’s experience indicates that resilience increasingly depends on institutional and logistical capacity: the ability to redirect supply chains within weeks, recalibrate refinery output without rebuilding plants, coordinate across ministries handling shipping, finance, and external affairs, and verify distribution digitally to forestall panic-driven hoarding. The vessels that sailed out of the Gulf for India at the height of the conflict reflected not chance but sustained diplomatic engagement with Saudi Aramco, ADNOC, and QatarEnergy maintained over years rather than weeks (Ministry of Petroleum and Natural Gas, interview, 2026). This is the conceptual shift worth naming: from energy security defined by what a country holds underground or in storage tanks, toward energy security defined by what a country can coordinate, redirect, and absorb under stress.

Table 2. India’s Energy Preparedness Before and During the Hormuz Crisis

| Indicator | Pre-Crisis | During Crisis | Strategic Significance |

| Crude supplier countries | ~27 (a decade earlier) | 40+ by 2026 | Reduced single-source concentration risk |

| Hormuz share of crude imports | ~45% | ~30% (non-Hormuz rose 55%→70%) | Rapid reallocation cushioned the chokepoint shock |

| Domestic LPG production | ~35,000 tonnes/day | ~54,000 tonnes/day within 8 days | Refinery flexibility substituted for lost Gulf cargoes |

| Strategic petroleum reserves | 5.33 million tonnes (~9.5 days) | Drawn down selectively; expansion announced at Chandikhol, Padur | Provided a buffer despite being below the IEA 90-day norm |

| City gas distribution cities | Expanding network | ~300 cities; LPG-to-PNG switching encouraged | Demand-side substitution eased LPG import pressure |

| Retail fuel price increase | Stable for 18+ months prior | ~7%, vs. ~25–30% global average | Fiscal absorption (excise cuts, OMC under-recoveries) shielded consumers |

Source: Ministry of Petroleum and Natural Gas, Government of India, interview transcripts; Indian Strategic Petroleum Reserves Limited (2026).

Conclusion

India avoided a severe energy crisis not because it was less exposed than Japan, Germany, or South Korea, but because that exposure was offset by institutional readiness accumulated over ten years of refinery upgrades, supplier diversification, and digital governance. The broader lesson for energy-importing economies is that resilience cannot be assembled during a crisis; it must be built well before one. Stockpiles buy time. Institutions buy adaptability. The Hormuz crisis did not spare India—it tested an architecture that had quietly been under construction long before the first missile was fired.

References:

Al Jazeera. 2026. “Which Countries Have Strategic Oil Reserves – and How Much?” Al Jazeera, March 23, 2026.

Ashok, B. (Former Chairman, Indian Oil Corporation Limited). 2026. Interview transcript: “How Did India Successfully Navigate the Strait of Hormuz Global Energy Crisis?”

Atlantic Council, Global Energy Center. 2026. “India’s Energy Security at a Crossroads: The Hormuz Crisis and an Opportunity for US-India Cooperation.” Atlantic Council.

Congressional Research Service. 2026. “Iran Conflict and the Strait of Hormuz: Impacts on Oil, Gas, and Other Commodities.” Washington, DC: Library of Congress.

Indian Strategic Petroleum Reserves Limited (ISPRL). 2026. Strategic petroleum reserve capacity data, cited in government interview transcripts.

Ministry of Petroleum and Natural Gas, Government of India. 2026. Interview transcripts and press briefings on India’s energy resilience during the Strait of Hormuz crisis.

Statista. 2026. “Chart: How Long Would Countries’ Oil Stocks Last?” Statista, March 25, 2026, based on International Energy Agency data.

U.S. Energy Information Administration (EIA). 2024. “The Strait of Hormuz Is the World’s Most Important Oil Chokepoint.” Washington, DC: EIA.

U.S. Energy Information Administration (EIA). 2026. “China, the United States, and Japan Hold Most Strategic Oil Inventories in 2025.” Washington, DC: EIA, April 20, 2026.

WION. 2026. “Global Strategic Oil Reserves Explained: How Long US, China, Japan, Germany, France, Italy and UK Can Survive an Oil Supply Crisis.” WION News.