India’s Energy Diplomacy in an Age of War, Sanctions and Strategic Fragmentation

Introduction: The Puzzle of the Non-Aligned Buyer

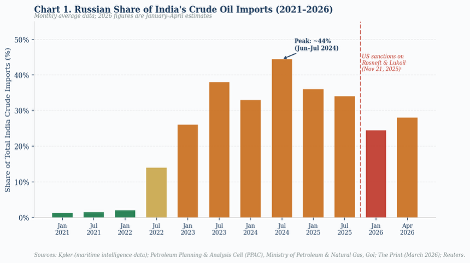

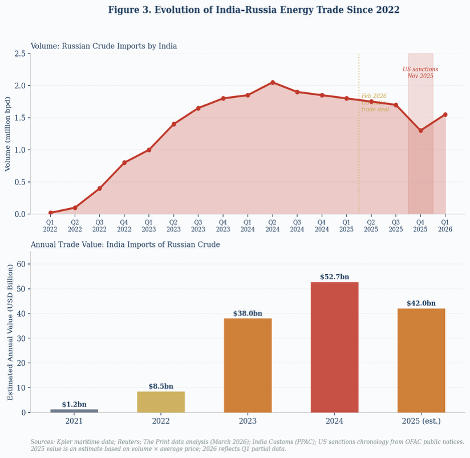

In February 2026, under a framework agreement that cut American tariffs on Indian exports from 50 per cent to 18 per cent, New Delhi made a significant diplomatic concession: it agreed to substantially reduce purchases of Russian crude oil. What followed confounded observers who had predicted Indian capitulation. Russia remained India’s single largest crude supplier through April 2026, with volumes recovering to approximately 2.15 million barrels per day as discounts widened again after months of disruption caused by US sanctions imposed in November 2025. The tariff deal offered relief; the oil trade continued, recalibrated rather than abandoned.

This sequence captures the central puzzle of Indian energy diplomacy: at a time when geopolitical polarisation is intensifying and great powers increasingly demand strategic alignment as a precondition for access, how has India simultaneously expanded energy ties with sanctioned Russia, preserved partnerships with Gulf monarchies, improved relations with Washington, and yet avoided structural dependence on any single patron? The answer reveals something analytically important about twenty-first-century power politics. Modern geopolitical influence rarely operates through coups or embargoes. It operates through shaping the environment within which sovereign states make economic decisions — and India’s energy strategy has become a sophisticated, documented exercise in resisting precisely that shaping.

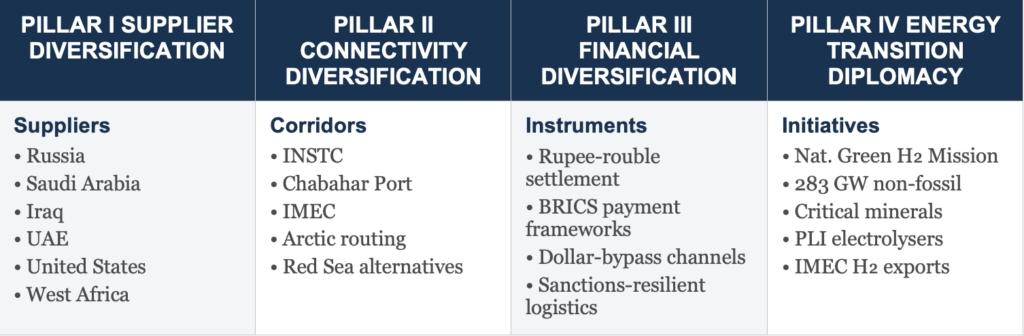

India’s energy diplomacy has evolved from resource procurement into a model of geopolitical hedging that sustains strategic autonomy through four interlocking pillars: supplier diversification, connectivity investment, financial engineering, and energy-transition diplomacy.

This article argues that India’s energy diplomacy has evolved from resource procurement into a model of geopolitical hedging that sustains strategic autonomy through four interlocking pillars: supplier diversification, connectivity investment, financial engineering, and energy-transition diplomacy. It further argues that the durability of this model depends on India’s capacity to close the structural gaps that each crisis has exposed — before the next one arrives.

Section I: The Russia Arbitrage — Gains, Costs and a Recalibration Forced by Sanctions

Before February 2022, Russia supplied less than two per cent of India’s crude imports. By June 2024, Kpler data showed Russia’s share peaking at approximately 44 per cent of India’s total crude intake, with daily volumes reaching 2.15–2.2 million barrels per day. The economics were straightforward: at the height of Western sanctions pressure in 2022–23, Urals crude traded at discounts of $8–10 per barrel against Brent on a delivered basis. India’s high-complexity private and state-owned refineries — Reliance, Nayara, Indian Oil, BPCL — processed discounted Russian barrels into refined products subsequently exported to global markets, including, paradoxically, to Europe itself. The resulting refining arbitrage protected domestic consumers: diesel prices in India rose only 3 per cent between late 2021 and late 2022, compared with increases of 25 to 36 per cent across Western nations.

The comparison with Europe is analytically instructive. European nations — whose collective Russian gas dependence pre-2022 dwarfed India’s oil exposure in relative terms — dismantled that dependence under political compulsion, absorbing severe industrial and inflationary costs. India, operating without alliance obligations requiring conformity with sanctions regimes, managed a far more orderly diversification, substituting Russian volumes with Middle Eastern and American grades precisely as discounts narrowed rather than under coercive deadline. Non-alignment, in energy terms, provided flexibility that alliance membership structurally denied.

Yet the arbitrage carried compounding risks. US sanctions on Rosneft and Lukoil, effective 21 November 2025, forced Indian refiners to reassess. Russian crude’s share in India’s import mix fell below 25 per cent for the first time in two years by February 2026, according to Kpler. India’s reliance on Russia’s “shadow fleet” of non-Western-insured tankers introduced operational fragility that no amount of diplomatic flexibility could fully resolve. Western powers sanctioned approximately 35 per cent of the shadow fleet. France detained the tanker Boracay carrying Urals crude destined for India’s Vadinar port. The logistics framework that had enabled India’s arbitrage proved vulnerable to targeted enforcement at chokepoints neither India nor Russia controlled.

The February 2026 US-India interim trade agreement brought partial resolution. Punitive tariffs were cut from 50 per cent to 18 per cent, removing Washington’s most potent economic lever. India committed to gradual diversification toward American and other non-Russian suppliers, with US crude imports already having nearly doubled in January–April 2026 to approximately 247,000 barrels per day, up from an average of 199,000 in 2024, per S&P Global Commodity Insights. Crucially, Commerce Secretary B.V.R. Subrahmanyam clarified that the goods India committed to purchasing — crude oil, LNG, defence equipment, ICT hardware — were already part of its regular import basket, reframing the concession as redirection rather than capitulation. Russia’s recovery to 2.15 million barrels per day by April 2026 confirmed that the recalibration was managed rather than structural.

Table 1. India’s Major Crude Oil Suppliers: FY2021–22 to Early 2026

| Supplier | Share FY2021–22 | Share FY2023–24 (Peak) | Share Jan–Apr 2026* | Strategic Role |

| Russia | <2% | ~44% (Jun 2024) | ~25–30% | Discount arbitrage; sanctions hedge |

| Iraq | ~22% | ~18% | ~18–20% | Term contracts; price anchor |

| Saudi Arabia | ~18% | ~16% | ~16–18% | OPEC reliability; ARAMCO ties |

| UAE | ~6% | ~5% | ~6% | Investment; IMEC node |

| United States | <1% | ~4% (2024 avg) | ~6.6% | Trade deal leverage; LNG growth |

| Others | ~52% | ~13% | ~18% | Diversification buffer |

Chart 1. Russian Share of India’s Crude Oil Imports (2021–2026)

Section II: The Gulf’s Enduring Weight — and the Limits of Proximity

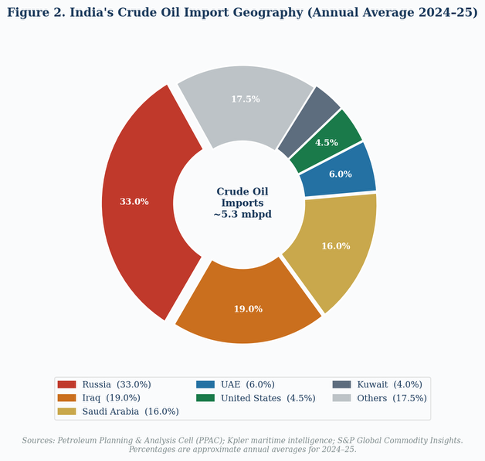

The Gulf’s centrality in India’s energy architecture long predates the Russia pivot and will long outlast it. Saudi Arabia, Iraq, and the UAE collectively supply roughly 50 per cent of India’s crude imports through term contracts, providing a price anchor and logistics reliability that spot market purchases of Russian Urals cannot replicate. The relationship has deepened beyond hydrocarbons: a 9-million-strong Indian diaspora in GCC states remits over $60 billion annually to India, Saudi Arabia’s Public Investment Fund has committed capital to Indian infrastructure sectors, and UAE’s Comprehensive Economic Partnership Agreement, concluded in 2022, provides preferential trade access that reinforces bilateral energy ties with commercial architecture.

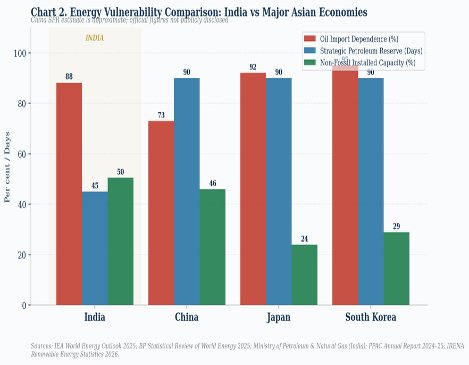

A comparison with China sharpens the strategic picture. Beijing purchases approximately 90 per cent of Iranian oil exports and has developed a protected financial corridor with Tehran that partially insulates those flows from Western enforcement. Yet China’s Gulf exposure is structurally similar to India’s: both economies depend on the Strait of Hormuz for the majority of their crude imports, and both face the same chokepoint vulnerability. The asymmetry lies in reserves and alternatives. China’s strategic petroleum reserves are estimated at over 90 days of consumption; India’s hover around 45 days. The conclusion is not that India’s Gulf strategy is deficient, but that its strategic depth behind that strategy requires reinforcement.

India’s Chabahar investment — $500 million committed for port development — illustrates the tension between connectivity ambition and sanctions vulnerability. The port offers India a non-Pakistani overland route to Afghanistan and Central Asia, directly advancing the INSTC’s strategic logic. Yet repeated US sanctions waivers, most recently extended only to April 2026 before renewed uncertainty, demonstrate that the corridor’s operational continuity depends on American forbearance rather than Indian sovereign choice. The Chabahar dilemma — strategically essential, diplomatically precarious — encapsulates the central challenge of India’s multi-vector energy architecture.

Figure 2. India’s Crude Oil Import Geography (Annual Average 2024–25)

Chart 2. Energy Vulnerability Comparison: India vs Major Asian Economies

Table 2. Comparative Energy Vulnerability Matrix: India, China, EU-27, Japan

| Economy | Oil Import Dependence | Primary High-Risk Supplier | Strategic Reserve (Days) | Hormuz Exposure | Energy Transition |

| India | ~88% | Russia / Gulf | ~45 | HIGH | 283 GW non-fossil (Mar 2026) |

| China | ~73% | Russia / Gulf | ~90+ | HIGH | World’s largest RE installer |

| EU-27 | ~97% | Norway / LNG | ~90+ | MEDIUM | REPowerEU; post-Ukraine acceleration |

| Japan | ~92% | Gulf (90%+) | ~90+ | HIGH | Slow; nuclear restart underway |

Section III: The Four-Pillar Framework — Architecture, Evidence and Gaps

Pillar Framework: supplier diversification, connectivity diversification, financial diversification, and energy-transition diplomacy. Each pillar addresses a distinct dimension of strategic autonomy; together they constitute a hedging model with no close precedent among comparably sized developing economies.

Figure 1. India’s Four-Pillar Energy Diplomacy Framework (Author’s Analytical Framework)

Pillar I — Supplier Diversification — is the most visible and best-documented. India now sources crude from over 40 countries, including Russia, Iraq, Saudi Arabia, UAE, the United States, West Africa, and Latin America. The deliberate maintenance of concurrent relationships with sanctioned and non-sanctioned suppliers is itself a policy instrument: it preserves competitive pricing tension among suppliers and denies any single power the leverage of indispensability.

Pillar II — Connectivity Diversification — has advanced less uniformly. The International North-South Transport Corridor (INSTC) reduces the Mumbai-Moscow freight distance by approximately 40 per cent compared to the Suez Canal route. The India-Middle East-Europe Economic Corridor (IMEC), endorsed at the September 2023 G20 Summit, could eventually carry green hydrogen to European industrial markets. INSTC and IMEC are analytically complementary: INSTC maximises India’s strategic depth northward through Russia and Iran; IMEC anchors westward commercial connectivity through the Gulf and Mediterranean. Neither is fully operational, and Chabahar’s sanctions vulnerability constrains INSTC’s land component.

Pillar III — Financial Diversification — addresses the invisible infrastructure of energy security. The Reserve Bank of India’s clearance of a rupee-rouble settlement pathway enables large-volume commodity trade outside dollar-denominated SWIFT transactions. The mechanism remains imperfect, but the precedent has been established at scale, raising the cost of financial coercion for Washington. BRICS-plus payment architecture discussions remain far from operational maturity.

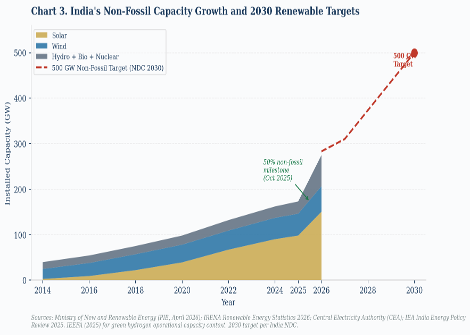

Pillar IV — Energy Transition Diplomacy — is the most consequential over a 10–20 year horizon. India’s non-fossil installed capacity reached 283.46 GW by March 2026 — an increase of 3.59 times since 2014, with 55.3 GW added in FY2025–26 alone, the highest annual addition on record (Ministry of New and Renewable Energy, April 2026). India crossed 50 per cent non-fossil installed capacity in October 2025, five years ahead of its NDC commitment. Yet the National Green Hydrogen Mission’s 2030 target remains imperilled: IEEFA analysis as of August 2025 found 94 per cent of announced green hydrogen capacity had yet to move beyond the announcement stage, and only 2.8 per cent was operational.

Chart 3. India’s Non-Fossil Capacity Growth and 2030 Renewable Targets

Section IV: The Geoeconomics of Financial Decoupling

The least visible but increasingly decisive dimension of India’s energy strategy concerns financial infrastructure. The Western sanctions regime targeting Russia operates primarily through three mechanisms: SWIFT exclusion, insurance denial (G7 P&I restrictions), and the $60-per-barrel G7 price cap. India’s navigation of all three has been partially successful but has generated compounding risks that financial engineering alone cannot resolve.

The rupee-rouble settlement channel bypasses SWIFT for bilateral oil transactions, establishing a precedent with implications beyond the Russia trade. When combined with India’s role in BRICS financial discussions — where India has cautiously engaged with proposals for alternative payment messaging without endorsing full dollar displacement — New Delhi has signalled that the architecture of Western financial leverage is contestable. The strategic significance is not that India has built a functional alternative to SWIFT; it has not. The significance is that a $4-trillion economy with deep US investment and trade relationships has demonstrated willingness to invest in bypass infrastructure, raising the cost of financial coercion for Washington.

European institutions, bound by sanctions compliance obligations, had no analogous bypass option when Russian gas was disrupted. Their energy adjustment was therefore primarily physical and supply-side: rapid LNG procurement, emergency storage, demand reduction, and politically managed industrial contraction. India’s financial flexibility enabled a different adjustment sequence — primarily price-side and demand-driven, managed over time rather than under crisis compulsion. The asymmetry reflects not just strategic choice but structural capacity.

Section V: Energy Transition as Strategic Competition

India’s clean energy ambitions are equally, and perhaps more consequentially, an industrial and geopolitical strategy. China’s dominance of global solar PV manufacturing (over 80 per cent of module capacity), lithium-ion batteries, and increasingly electrolysers means that any nation pursuing rapid renewable deployment without domestic manufacturing capacity risks substituting hydrocarbon import dependence for clean technology import dependence. India’s Production-Linked Incentive scheme for solar modules has already built module and cell production capacity of approximately 80 GW and 7 GW respectively as of March 2025, with projections of 110 GW module capacity by 2026 (Carbon Brief, 2025; IEEFA, 2025) — making India the world’s second-largest manufacturer. This is a direct industrial policy response to Chinese cleantech dominance.

Green hydrogen’s strategic logic extends further. The National Green Hydrogen Mission, backed by INR 197 billion ($2.2 billion) in budgeted outlay, targets sectors — fertilisers, steel, refineries — that currently consume imported natural gas and coal. IMEC provides a potential export corridor to European industrial decarbonisation markets: the EU’s Carbon Border Adjustment Mechanism creates structural demand for low-carbon industrial inputs, and India’s competitive renewable electricity costs position it as a credible supplier — if the infrastructure, demand mandates, and electrolyser cost curves align. The IEEFA assessment that 94 per cent of announced capacity remains unbuilt indicates that policy intervention is urgently required to prevent the mission from becoming aspiration without architecture.

Table 3. Major Geopolitical Risks to India’s Energy Security (2026–2030)

| Risk | Probability 2026–2030 | Potential Impact | Mitigation Pathway |

| Sustained Gulf/Hormuz supply disruption | Medium | Critical | SPR expansion to 90 days; INSTC operationalisation |

| Escalation of US secondary sanctions on Indian refiners | Medium | High | Feb 2026 trade deal buffers this; pivot to US/Gulf crude underway |

| China cornering critical mineral & cleantech supply chains | High | High | PLI manufacturing scale-up; mineral diplomacy in Africa/Central Asia |

| Shadow fleet collapse under Western enforcement | Medium | High | Accelerated Gulf/US diversification already triggered post-Nov 2025 |

| Green hydrogen 2030 target miss | High | Medium | Demand mandates; purchase obligations; infrastructure investment |

Section VI: Strategic Forecasting to 2030

Best Case

The February 2026 trade framework matures into a full US-India bilateral trade agreement by late 2026, reducing tariff exposure to 15 per cent and creating a pathway for American investment in India’s clean energy manufacturing. Russia’s share in Indian imports stabilises at 20–25 per cent through managed diversification. INSTC achieves partial commercial operationalisation via alternative Azerbaijani routing. Green hydrogen demand mandates and purchase obligations, introduced by 2027, accelerate project commissioning toward 2–3 MMT annual production by 2030. By 2028–30, India’s non-fossil capacity reaches 400 GW and oil import dependence falls to 75 per cent.

Most Likely Case

India maintains a managed Russian crude share of 25–30 per cent, with diversification to US, Gulf, and West African suppliers proceeding as discounts narrow. The trade deal remains an interim framework, subject to periodic renegotiation. Green hydrogen misses the 2030 target by 40–50 per cent but establishes a viable domestic production base of 2–3 MMT. INSTC remains partially operational. India’s strategic autonomy is preserved at increasing fiscal and diplomatic cost as the management overhead of multi-alignment rises with geopolitical fragmentation.

Worst Case

Escalation of US secondary sanctions targeting Indian refiners forces an abrupt diversification that drives domestic fuel price increases and inflation. Simultaneously, a structural disruption in Gulf supply exposes the inadequacy of India’s 45-day strategic petroleum reserves. Clean energy transition falls behind schedule, deepening coal dependence. China secures preferential supply relationships with both Russia and Gulf producers simultaneously. India is forced into de facto alignment with one bloc, surrendering the strategic flexibility that has defined its post-1991 foreign policy posture.

The Strongest Critique: Is Multi-Alignment Fiscally Sustainable?

The most substantive critique of India’s hedging strategy is not that it fails strategically but that it is increasingly expensive operationally. Managing simultaneous relationships with Washington, Moscow, Riyadh, Brussels, and Beijing requires continuous diplomatic bandwidth, financial engineering, and willingness to absorb friction costs. Critics argue that multi-alignment is a posture viable for rising powers in periods of geopolitical fluidity but becomes progressively more costly as polarisation sharpens.

The critique has merit but underestimates the comparative cost of alignment. Europe’s gas dependency, dismantled only through severe economic adjustment, illustrates what alignment-induced energy vulnerability costs when geopolitical conditions shift. Japan’s near-total Gulf dependence — with over 90 per cent of oil imports traversing the Strait of Hormuz and no comparable diversification architecture — presents the alternative model. India’s approach is not cost-free; it is, however, demonstrably less costly than the structural vulnerabilities alignment would entail.

Policy Recommendations

Immediate Priorities (6–12 Months)

India should formalize a Chabahar sanctions carve-out within the evolving US-India trade framework, positioning the corridor as essential to Indo-Pacific connectivity and humanitarian logistics. Strategic petroleum reserves should be programmed for expansion from 45 to 90 days of consumption coverage, prioritising crude grade diversification to include non-Hormuz-dependent sources. The government should introduce formal demand mandates for green hydrogen procurement by public sector fertiliser and refinery consumers, providing the demand signal that IEEFA identifies as the primary barrier to project commissioning.

Medium-Term Priorities (1–5 Years)

INSTC’s commercial operationalisation requires investment in Caspian and Iranian port infrastructure alongside development of Indian-owned logistics entities capable of operating under sanctions uncertainty. The rupee-rouble settlement mechanism should be supplemented by engagement with UAE and Saudi Arabia to develop a multi-currency Gulf energy settlement framework. Domestic electrolyser manufacturing under PLI schemes should target 5 GW of annual production capacity by 2028 to underpin NGHM targets. Critical mineral partnership agreements with at least five African and Central Asian producers should be concluded, offering infrastructure investment in exchange for long-term lithium, cobalt, and rare earth offtake.

Long-Term Priorities (5–15 Years)

By 2035, India should target a structural reduction in oil import dependence from the current 88 per cent of total energy consumption to below 70 per cent, achieved through EV adoption at scale, green hydrogen deployment in hard-to-abate sectors, and ethanol blending. India should seek to institutionalise the International Solar Alliance into a broader Global South energy security framework, giving developing economies collective bargaining capacity in both fossil fuel and clean energy markets. At current import volumes, a 15 percentage-point reduction in oil import dependence would represent structural savings comparable to India’s entire annual defence budget.

Conclusion: Energy as Strategic Sovereignty

India’s energy strategy since 2022 constitutes a live experiment in twenty-first-century geopolitical hedging. It demonstrates that energy security is no longer primarily determined by who controls oil reserves or pipelines; it is determined by diplomatic flexibility, payment system resilience, connectivity architecture, and the capacity to indigenise the technologies that will define the next energy order. Russia’s vast hydrocarbon wealth did not prevent Moscow from becoming dependent on a narrowing circle of buyers. Europe’s sophisticated financial infrastructure did not prevent German industry from absorbing the cost of pipeline disruption. India’s insistence on strategic optionality — managing Washington’s pressure, Moscow’s discount offers, Riyadh’s partnership, and Brussels’ green standards simultaneously — has preserved flexibility at a cost that has proven, to date, manageable.

The vulnerabilities are real and structural: 45 days of strategic petroleum reserves against Japan and China’s 90-plus; a green hydrogen mission where only 2.8 per cent of announced capacity is operational; a connectivity corridor whose most strategically valuable component runs through a sanctions-constrained country. Closing these gaps — before the next crisis rather than within it — is the central task of Indian energy statecraft for the remainder of this decade.

In an era of strategic fragmentation, energy autonomy is not purchased by oil reserves or pipelines alone. It is built, piece by piece, through the unglamorous work of payment architecture, connectivity investment, and industrial policy — the infrastructure of a sovereignty that cannot be sanctioned away.