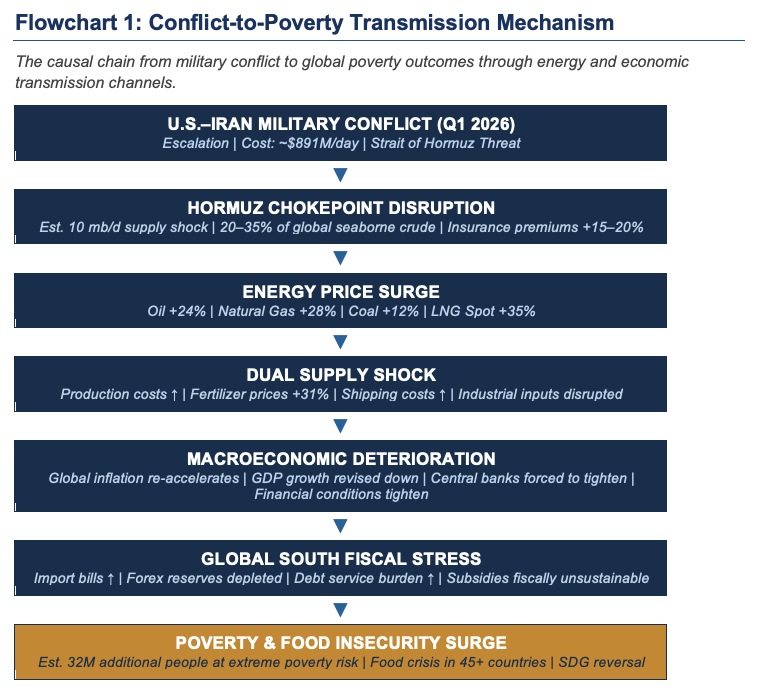

The escalation of the U.S.–Iran conflict in early 2026 has transitioned from a localized security crisis to a systemic reset of the international economic order. This paper provides a comprehensive, data-driven analysis of the transmission channels through which the conflict propagates—centered on the Strait of Hormuz, the world’s most critical maritime chokepoint. With approximately 20–35% of global seaborne crude oil trade transiting the Strait, the current disruption of an estimated 10 million barrels per day (mb/d) represents the most severe oil supply shock in recorded history. The resulting inflationary pressure has driven energy prices up by approximately 24% and fertilizer costs by approximately 31% in 2026 alone, consistent with World Bank Commodity Markets projections. Utilizing data from the World Bank, IMF, and IEA, this paper demonstrates that the conflict is accelerating the fragmentation of the global trade system into rival geoeconomic blocs. The analysis highlights a critical vulnerability in the Global South, where input shortages and high sovereign debt have placed an estimated 32 million additional people at risk of extreme poverty (consistent with World Bank poverty modeling). The paper concludes with a tripartite policy framework aimed at mitigating immediate shocks while fostering a more resilient international financial architecture.

1. Introduction: The Geopolitics of Systemic Vulnerability

As of May 2026, the global economy is navigating what international institutions characterize as a “polycrisis”—a confluence of overlapping shocks where the impact of each crisis is amplified by the existence of others. The U.S.–Iran conflict has evolved from a regional standoff into the primary determinant of global macroeconomic stability, with military operations alone estimated to cost approximately $891 million per day for the U.S. and its allies (IEGI Research Division, 2026).

The conflict erupted at a moment of extreme global fragility. Prior to the escalation, the World Bank warned that global growth was already projected to slow to 2.4%—the third consecutive year of deceleration (World Bank Global Economic Prospects, 2024). Against this backdrop, the effective closure or severe restriction of the Strait of Hormuz has created a physical shortage that transcends mere price volatility.

The Strait of Hormuz handles between 20% and 35% of all global seaborne crude oil trade, and nearly 30% of global fertilizer inputs originate in the Gulf region (IEA; IEGI, 2026). The world is now navigating a historic transition from efficiency-based globalization toward security-based fragmentation—a structural shift with consequences extending decades beyond any ceasefire.

2. Theoretical Framework: Geoeconomics and Supply Shock Theory

The current crisis is not a standard business cycle downturn; it is a geoeconomic rupture. Geoeconomics—the deployment of economic instruments for strategic geopolitical purposes—has replaced the traditional liberal trade model as the primary frame through which states and firms make investment, production, and procurement decisions (Klement, 2021).

2.1 The Geoeconomic Paradigm

The U.S.–Iran conflict serves as a case study for systemic unpreparedness for non-market forms of economic governance. As Collins (2025) observes, the rules of international economic law are increasingly perceived as “no longer fit for purpose” as supply chains reorganize along geopolitical rather than efficiency axes.

This paradigm shift has three structural dimensions: (1) the weaponization of resource chokepoints as instruments of coercive statecraft; (2) the deliberate fragmentation of multilateral trade institutions into competing plurilateral blocs; and (3) the emergence of “security premiums” embedded permanently into the cost of global commerce.

2.2 Dual-Channel Supply Shock Dynamics

The conflict triggers a dual-channel supply shock. The first channel operates through direct energy costs—the immediate pass-through of higher crude prices to transportation, manufacturing, and household energy budgets globally. The second, more pernicious channel operates through production cost shocks: rising input prices for fertilizers, industrial gases, and petrochemical derivatives reduce agricultural yields, disrupt semiconductor manufacturing, and constrain capital investment (Legrand, 2022).

Unlike demand-side shocks, supply-side disruptions force central banks into a deeply uncomfortable trade-off between combating inflation (requiring rate increases) and protecting economic growth (requiring monetary accommodation). The IMF has characterized this dynamic as a “stagflationary trap”—a condition where both growth and purchasing power deteriorate simultaneously (IMF World Economic Outlook, 2022).

Table 1: Geoeconomic Vulnerability Index by Economic Bloc (2026)

| Economic Bloc | Energy Import Dependency | Fertilizer Exposure | Fiscal Buffer Status | Stagflation Risk |

| OECD Economies | ~65% | Moderate | Adequate–High | Moderate |

| Emerging Asia | ~72% | High | Variable | High |

| Sub-Saharan Africa | ~80% | Critical | Depleted | Severe |

| Latin America | ~55% | Moderate–High | Constrained | Elevated |

| MENA (non-GCC) | ~60% | High | Constrained | High |

3. Energy Shock Analysis: The Hormuz Chokepoint

The Strait of Hormuz—a 33-kilometer-wide waterway between Iran and Oman—constitutes the single most consequential chokepoint in global energy infrastructure. Its closure or severe disruption creates bottlenecks that ripple through every layer of the global economy, from retail fuel prices to sovereign debt dynamics.

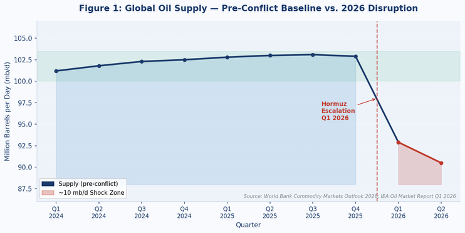

3.1 The 10 Million Barrel/Day Disruption

The current disruption of an estimated 10 mb/d represents the largest oil supply shock on record, exceeding the 1973 Arab Oil Embargo (approximately 4.3 mb/d) and the 1979 Iranian Revolution (approximately 5.6 mb/d) (IEA historical data; IEGI, 2026). Three transmission mechanisms are operative:

Price Escalation: Brent crude oil, which had stabilized at approximately $85–90 per barrel in late 2025, surged following the escalation, averaging approximately $100 per barrel since conflict onset, with spot prices reaching significantly higher as commercial stockpiles deplete.

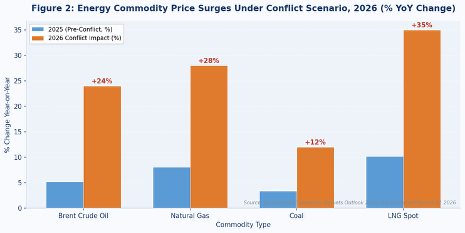

Energy Price Cascade: Overall energy prices are projected to surge by approximately 24% in 2026—their highest level since the 2022 post-Ukraine energy crisis. Natural gas prices are experiencing an even steeper increase of approximately 28%, with coal rising approximately 12% as substitution demand accelerates (World Bank Commodity Markets Outlook; IEGI, 2026).

Maritime Insurance Premium: Rising maritime insurance premiums and growing insurer reluctance to cover vessels transiting the Gulf region have added a “security premium” of an estimated 15–20% to shipping costs, further inflating delivered commodity prices (IEGI, 2026).

3.2 Strategic Reserve Limitations

International Energy Agency (IEA) member countries collectively hold approximately 1.5 billion barrels in strategic petroleum reserves, representing roughly 90 days of net import cover. A protracted Hormuz disruption lasting 60 or more days would rapidly erode this buffer. The IEA coordinated two emergency reserve releases in 2022 (post-Ukraine) totaling approximately 240 million barrels; a comparable or larger intervention would be required in the current scenario, with diminishing effect if disruption persists (Beccue and Huntington, 2016).

4. Supply Chain Disruptions: Fertilizers, Food, and Industrial Inputs

The conflict is not solely an energy crisis; it constitutes a compound industrial and agricultural input crisis. The Gulf region is a critical origin point for petrochemical derivatives and industrial gases that underpin global manufacturing and food production.

4.1 The Fertilizer Price Nexus

Approximately 30% of the world’s nitrogen fertilizer inputs originate in the Gulf region, where abundant natural gas serves as the primary feedstock for ammonia and urea production (IEGI, 2026; World Bank). The conflict-driven gas supply disruption has triggered a structural price shock:

Urea Prices: Fertilizer prices are projected to increase by approximately 31% in 2026, driven substantially by an estimated 60% jump in urea prices (IEGI, 2026; consistent with FAO Food Price Index trends).

The Crop Calendar Trap: Because fertilizer application must align with specific, non-negotiable crop calendars, input shortages in early 2026 will translate into lower yields in late 2026 and throughout 2027—creating a “time bomb” for food security, with the most severe consequences in Sub-Saharan Africa and South Asia (IEGI, 2026; World Food Programme).

Food Price Inflation: The FAO Food Price Index, which had stabilized following the 2022 Ukraine-driven spike, is again under significant upward pressure, particularly for wheat, rice, and palm oil.

4.2 Industrial Inputs and Technology Supply Chains

The conflict disrupts the supply of critical by-products of oil and gas refining, including helium (essential for semiconductor cooling), sulfur (essential for phosphate fertilizers and battery production), and various petrochemical precursors for plastics and pharmaceuticals (IEGI, 2026). The semiconductor industry faces a compounded exposure: rising electricity costs in key Asian manufacturing economies—notably Taiwan, South Korea, and Japan—threaten production economics across the chip supply chain, with feedback loops reaching the ~$650 billion in AI infrastructure investment contemplated by major technology companies (IEGI, 2026).

Table 2: Critical Supply Chain Dependencies — Gulf Region Exposure and 2026 Price Impact

| Input Type | Gulf Export Share | Est. 2026 Price Surge | Primary Impact Sector | Recovery Timeline |

| Crude Oil / LNG | ~20–35% of seaborne | +24% / +28% | All sectors (universal) | Conflict-dependent |

| Urea / Ammonia | ~30% of global supply | +60% | Global agriculture | 12–18 months post-conflict |

| Helium | Significant (Qatar/Iran) | +30%+ | Semiconductors, Medical | 6–12 months |

| Sulfur | Significant (Gulf) | +25%+ | Phosphate fertilizers, Batteries | 6–12 months |

| Petrochemical Precursors | ~25% of global trade | +20–35% | Pharma, Plastics, Chemicals | 12–24 months |

5. Macroeconomic Impact: Inflation, Stagflation, and GDP Slowdown

The IMF has revised its global growth expectations downward as a direct consequence of the conflict. The combination of supply-side energy shocks, tightening financial conditions, and heightened geopolitical uncertainty is producing a synchronized global deceleration—with disproportionate severity in emerging market and developing economies (EMDEs).

5.1 Global Growth Downgrades

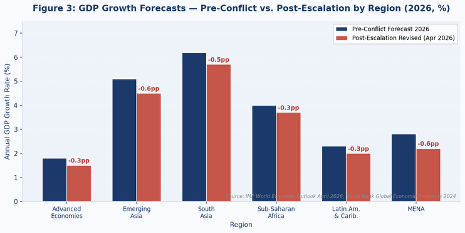

Prior to the conflict, the World Bank projected global growth of 2.4% for 2026—already described as “anemic” (World Bank Global Economic Prospects, 2024). The conflict has prompted further IMF downward revisions across all regions:

Emerging Asia: Growth expectations revised down by approximately 0.6 percentage points (consistent with IMF April 2026 World Economic Outlook).

Sub-Saharan Africa: Growth cut by approximately 0.3 percentage points—a significant setback for a region where even marginal growth deceleration translates directly into poverty increases (IEGI, 2026).

Advanced Economies: Growth downgrades of 0.2–0.4 percentage points, reflecting energy import costs, financial market volatility, and trade uncertainty (IMF World Economic Outlook, 2026).

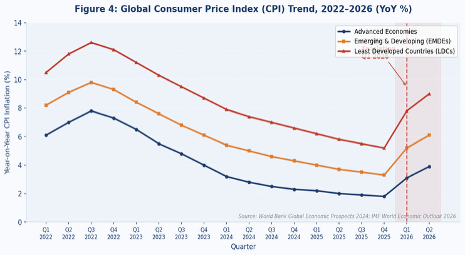

5.2 Inflation and Stagflation Dynamics

Global headline inflation, which had been gradually decelerating toward central bank targets through 2025, has re-accelerated sharply. The energy and food price transmission channels—operating with differing lags—create a multi-wave inflation pattern: an immediate energy price shock followed by a lagged food price surge, followed by a second-order core inflation impulse as energy costs permeate wage and production cost structures.

6. Impact on Developing Economies: Poverty, Inequality, and Debt Stress

The U.S.–Iran conflict hits the world’s most vulnerable populations hardest, compounding pre-existing structural fragilities. For low-income countries (LICs) and lower-middle-income countries (LMICs), the conflict constitutes a multidimensional shock: simultaneously an energy shock, a food security shock, a fiscal shock, and a financial stress event.

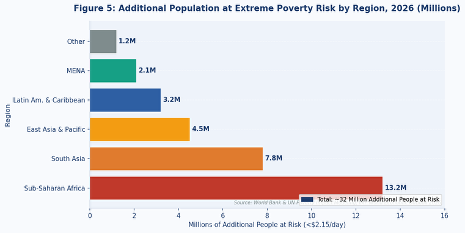

6.1 The 32 Million Poverty Projection

International agencies have warned of a systemic global poverty reversal. Consistent with World Bank modeling frameworks applied to analogous supply shocks, this disruption is projected to place approximately 32 million additional people at risk of extreme poverty (living on under $2.15/day in 2017 PPP terms), as food and energy inflation outpaces income growth for the poorest quintile (IEGI, 2026; UN, 2022). Key vulnerability dimensions include:

Energy Poverty Amplification: In economies such as Pakistan, Bangladesh, and several Sub-Saharan African nations, businesses and households are already enduring severe power cuts as natural gas availability deteriorates (IEGI, 2026).

Food Insecurity: The World Food Programme (WFP) has identified food insecurity hotspots across the Sahel, Horn of Africa, and Yemen acutely sensitive to fertilizer-driven food price increases. A 31% rise in fertilizer costs cascading into a 10–15% food price increase in already stressed markets constitutes a humanitarian emergency threshold.

Remittance Risk: For economies heavily dependent on remittances from GCC countries—including Egypt, Pakistan, the Philippines, and Bangladesh—the conflict introduces additional vulnerability: GCC economic contraction could reduce remittance flows, compounding domestic fiscal stress.

6.2 Sovereign Debt Stress and Currency Depreciation

Emerging economies face what Storm (2022) characterizes as “tighter financial conditions against a backdrop of high debt.” Countries with high external debt denominated in U.S. dollars face a double jeopardy: rising import costs AND dollar appreciation driven by safe-haven demand, simultaneously increasing the real burden of debt service. The stagflationary dynamic forces central banks in advanced economies to maintain or increase interest rates, transmitting tighter financial conditions globally and creating borrowing cost pressures for emerging market governments precisely when they most need fiscal space.

7. Policy Responses: Subsidies, Transfers, and Fiscal Limits

Policymakers across the income spectrum face deeply uncomfortable trade-offs between fiscal sustainability and social protection. The speed and severity of the shock have outpaced institutional preparedness of most governments, particularly in the Global South (World Bank, 2024).

7.1 The Subsidy Dilemma

Many governments have responded with fuel tax cuts, direct price subsidies, and controlled energy pricing. While these measures provide immediate household relief, they are fiscally unsustainable at scale and risk crowding out productive public investment. In low-income economies, where fiscal space is already severely constrained, the choice between maintaining subsidies and servicing debt represents an existential policy dilemma (Nguyen and Su, 2022).

A critical distinction exists between well-targeted cash transfers (generally superior in efficiency and fiscal terms) and broad-based energy subsidies (politically expedient but highly regressive). International financial institutions, including the IMF and World Bank, have consistently recommended the former; political economy pressures in crisis conditions have frequently produced the latter.

Table 3: Policy Response Comparison — Cost, Effectiveness, and Fiscal Risk

| Policy Instrument | Implementation Cost | Targeting Precision | Fiscal Impact | Political Feasibility |

| Universal Fuel Subsidies | Very High | Low (regressive) | Severe deficits | High (popular) |

| Targeted Cash Transfers | Moderate | High (progressive) | Manageable if phased | Moderate |

| Fuel Tax Cuts | Moderate–High | Low (broad) | Revenue reduction | High (popular) |

| Emergency Food Vouchers | Low–Moderate | High | Limited | High (targeted) |

| IMF Emergency Financing | Variable | N/A (sovereign) | Debt-creating | Conditional |

7.2 Advanced vs. Developing Economy Constraints

Advanced economies (AEs), possessing deeper capital markets, reserve currencies, and established welfare infrastructure, have deployed strategic reserve releases, windfall profit taxes on energy companies, targeted household rebates, and monetary policy coordination. Developing economies face a fundamentally different and more constrained landscape: limited domestic capital markets, currency vulnerability, high external debt, and weak social protection infrastructure—creating asymmetric capacity to respond to an identical shock.

8. Structural Shift in Globalization: Friend-Shoring and Bloc Formation

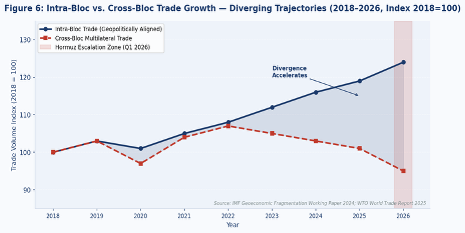

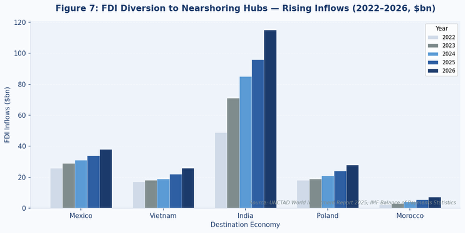

The U.S.–Iran conflict is functioning as a powerful catalyst for what analysts have termed “fragmented globalization”—a world in which trade, investment, and technology flows increasingly occur within geopolitically aligned blocs rather than across a unified multilateral system (Blagov, Dirks and Funke, 2024).

8.1 From “Just-in-Time” to “Just-in-Case”

The COVID-19 pandemic initiated a re-evaluation of lean, efficiency-maximizing supply chain models. The Ukraine conflict accelerated this reassessment. The Hormuz crisis may prove definitive: geopolitical risks are now primary determinants of firm-level investment and sourcing decisions. Businesses are actively relocating production capacity to politically aligned jurisdictions—“friend-shoring”—to de-risk their supply chains from adversarial geography (Blagov, Dirks and Funke, 2024).

8.2 Emerging Geoeconomic Blocs

Western Bloc (U.S.-led): Pursuing aggressive friend-shoring, CHIPS Act-style industrial policies, and the Inflation Reduction Act green energy transition. Strategic relationships with Canada, Australia, Japan, South Korea, and European allies are being deepened.

China-Russia-Iran Axis: Expanding bilateral trade in non-dollar currencies, developing alternative payment systems (including expanded use of the digital yuan), and positioning the Shanghai Cooperation Organisation (SCO) as an alternative economic architecture.

Non-Aligned South: The largest and most economically diverse grouping—comprising India, ASEAN nations, Gulf states, Africa, and much of Latin America—is strategically navigating between blocs, seeking the best terms from each. This group’s choices will largely determine whether fragmentation accelerates or is contained.

Critically, this fragmentation is not cost-free. IMF estimates suggest that deep geoeconomic fragmentation could permanently reduce global output by up to 7% of GDP in the long run—a loss larger than the combined annual output of Germany and Japan (IMF World Economic Outlook, 2023). The international legal system is correspondingly moving toward fragmented, bloc-based trade agreements, with the WTO’s dispute settlement mechanism increasingly sidelined (Collins, 2025).

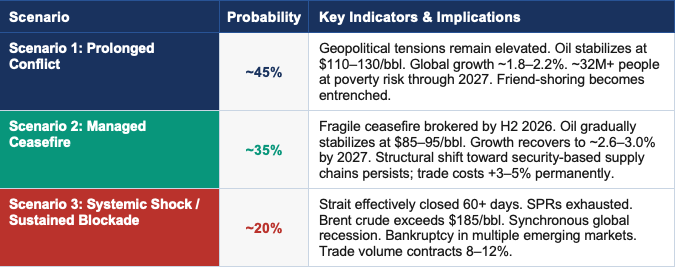

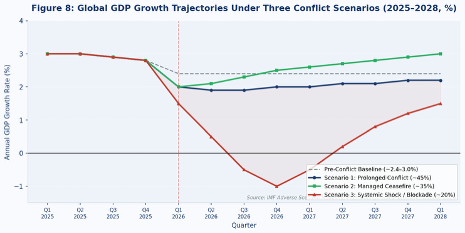

9. Scenario Analysis: 2026 and the Emerging Global Architecture

Three plausible scenarios define the range of outcomes over the 2026–2028 horizon. These are analytical constructs based on current trajectories and institutional signaling; they should not be interpreted as predictions.

Table 4: Scenario Analysis — 2026–2028 Outlook

10. Policy Recommendations

The following recommendations are organized into a tripartite framework: immediate crisis mitigation (0–6 months), medium-term structural stabilization (6–24 months), and long-term resilience architecture (2–10 years).

10.1 Short-Term: Crisis Mitigation (0–6 Months)

Coordinated IEA Emergency Reserve Release: Immediate release of strategic petroleum reserves by IEA member states—targeting a minimum of 150–200 million barrels over 90 days—to blunt the acute 10 mb/d shock and provide price stabilization (Beccue and Huntington, 2016).

G20 Emergency Fertilizer Financing Facility: Establish an emergency multilateral fund of $3–5 billion to subsidize fertilizer procurement for food-insecure nations facing crop calendar deadlines, modeled on the World Bank’s Global Food and Nutrition Security Crisis Response.

IMF Rapid Financing Instrument (RFI) Scale-Up: Expand IMF RFI access limits and expedite disbursement for the 15–20 most acutely stressed emerging market economies, preventing disorderly debt defaults.

Targeted Social Protection Corridors: Redirect fuel subsidy spending toward targeted, digitally-delivered cash transfers to the bottom two income quintiles, maximizing welfare impact per fiscal dollar.

10.2 Medium-Term: Structural Stabilization (6–24 Months)

Accelerated Debt Relief: Launch an expedited Common Framework restructuring for Pakistan, Sri Lanka, Egypt, and other economies whose fiscal buffers are critically depleted (Storm, 2022). Debt service suspension conditioned on social protection floor maintenance.

Alternative Supply Route Investment: G7 governments and multilateral development banks should co-finance accelerated development of alternative oil pipeline routes (UAE-Oman overland capacity, Saudi East-West pipeline) to reduce structural Hormuz dependency.

Agricultural Input Diversification: Support diversification of fertilizer supply chains through investment in African potash deposits, precision fermentation nitrogen alternatives, and soil health programs reducing input dependency.

10.3 Long-Term: Resilience Architecture (2–10 Years)

Reform of International Trade Law: As Collins (2025) argues, the existing WTO rulebook is inadequate for a world of strategic resource competition. A plurilateral “Geoeconomic Trade Code” governing critical materials and energy chokepoints would provide a more resilient foundation.

Accelerate Renewable Energy Transition: The conflict demonstrates the systemic fragility of fossil fuel dependency. Accelerating clean energy transition in both advanced and developing economies—with adequate technology transfer and financing for the Global South—is the most durable long-term remedy.

Strengthen Global Food Security Architecture: Operationalize a reformed WFP-FAO-World Bank integrated food security early warning and financing system, with pre-committed financing triggers activated by commodity price and supply shock indicators.

11. Conclusion

The U.S.–Iran conflict has exposed the deep structural vulnerabilities of a global economy organized around efficiency, interdependence, and the assumption of geopolitical stability. The Strait of Hormuz has become the most consequential chokepoint in the modern global economy—a 33-kilometer bottleneck through which flows the economic lifeblood of billions of people who have no direct stake in the conflict driving its disruption.

The transmission mechanism from military conflict to household poverty is not abstract; it is concrete, measurable, and accelerating. Energy price surges of +24%, fertilizer shocks of +31%, and an estimated 32 million additional people at risk of extreme poverty represent not projections but the early-stage manifestations of a shock whose full consequences will unfold over 2026–2028.

The structural transformation of globalization—from multilateral efficiency to plurilateral security—is the most consequential long-term consequence of the conflict. This transformation will permanently increase the cost of global commerce, widen inequality between blocs, and impose disproportionate burdens on the Global South, which lacks the institutional, financial, and military resources to shape the new architecture to its benefit.

The policy window for preventing the worst outcomes—a full-scale global recession, mass food insecurity events, and cascading emerging market debt defaults—remains open, but it is narrowing. The credibility of international institutions, from the IMF and World Bank to the WFP and IEA, will be defined by the speed and adequacy of their response in the coming months.

A conflict that began in the Strait of Hormuz is reshaping the foundations of the global economic order. The fundamental question is no longer whether the world will be more fragmented, more unequal, and more costly to navigate—it is whether the institutions built for the post-1945 era of open globalization can adapt rapidly enough to prevent a systemic collapse of the multilateral economic order.