It is not often that a nation finds itself at the cusp of a seismic shift in the global economic order. Yet, according to the latest Economy Watch report from EY, that is precisely where India stands today. If we keep our economic engines running at their current pace, by 2038 India will overtake the United States to become the world’s second-largest economy in purchasing power parity (PPP) terms—second only to China.

That would be more than a change in rankings. It would mark the arrival of a new economic heavyweight with the power to shape global markets, influence the rules of trade, and set the tone for the 21st century’s growth narrative.

Already a Global Giant in PPP Terms

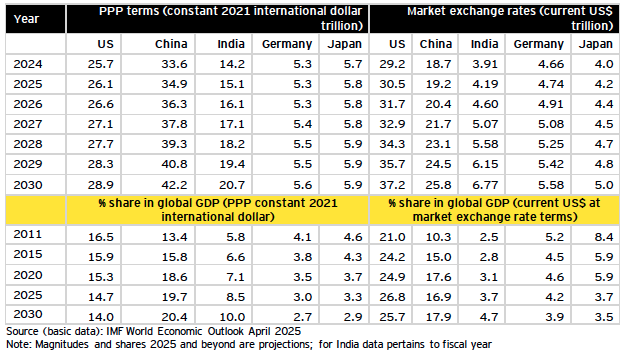

EY’s report makes one thing clear: India is not merely catching up; we’re already on the podium. In 2024, India’s GDP in PPP terms stood at $14.2 trillion, making us the third-largest economy in the world, behind China at $33.6 trillion and the US at $25.7 trillion.

This is more than an academic distinction. PPP adjusts for price differences between countries, reflecting the real size of an economy’s output and the living standards it can sustain. And on this measure, India already outweighs traditional economic powers like Japan and Germany by a wide margin.

In nominal GDP—measured at market exchange rates—India still has ground to cover, at around $3.9 trillion in 2024. But here, too, we are on the move. EY projects that India will overtake Japan in 2025 and surpass Germany by 2028, becoming the third-largest economy in nominal terms.

The 2038 Moment

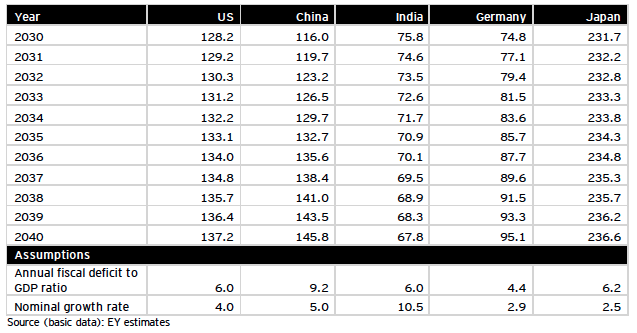

The big headline from EY’s analysis is the possibility that by 2038, India’s GDP could surpass that of the United States in PPP terms.

The math is straightforward but telling. Between 2028 and 2030, if India maintains an average growth rate of 6.5%—in line with IMF projections—and the US grows at 2.1%, the gap will close. By 2038, both economies are expected to be in the range of $32–33 trillion in constant 2021 PPP dollars, with India pulling ahead.

This isn’t wishful thinking. For much of the past decade, India’s growth rate has been more than double, and at times triple, that of the US. The advantage is structural, not cyclical.

Why India Has the Edge

Demographics: Our median age in 2025 is just 28.8 years, compared to 38.5 in the US, 40.1 in China, and nearly 50 in Japan. This “demographic dividend” means not just a larger workforce but decades of rising consumption, innovation, and entrepreneurship.

Investment Muscle: India’s gross capital formation—essentially investment in productive assets—averages 33.5% of GDP in nominal terms and 35.1% in real terms. That’s among the highest for any major economy, providing the physical and technological foundation for sustained growth.

Domestic Demand Strength: Unlike export-heavy economies such as Germany, India is powered primarily by domestic consumption, which accounts for over 70% of GDP. This makes us more resilient to global downturns and trade disruptions.

Policy Momentum: The report credits ongoing reforms—ranging from GST simplification to infrastructure-led capital expenditure—for boosting productivity and demand. Employment promotion schemes, rural demand revival, and a robust services sector add further thrust.

A Slowing World Around Us

Context matters. The OECD forecasts that advanced economies will grow far more slowly in the coming years. The US is expected to expand just 1.6% in 2025 and 1.5% in 2026. The Euro area, UK, and Japan will struggle to cross 1.5%. China’s growth, too, is projected to slow to 4.3% by 2026 due to structural headwinds and trade tensions.

In this landscape, India’s 6.3–6.5% projected growth stands out not as a statistical quirk but as a sustained divergence. Over time, that gap compounds into massive shifts in economic weight.

Risks on the Road

Of course, the road to 2038 is not without hazards. The most immediate comes from across the Pacific: higher US tariffs on select Indian exports. EY calculates that about 0.9% of India’s GDP is potentially exposed, with the direct hit to growth at around 0.3 percentage points. The good news? With targeted countermeasures—diversifying export markets, boosting domestic demand, and reducing import dependence—the impact could be cut to just 0.1%.

Other risks lurk in the background: volatile oil prices, climate shocks affecting agriculture, and the perennial challenge of sustaining reform momentum in a democracy as complex as ours.

The Structural Advantages No One Can Ignore

Debt Discipline: Among the world’s five largest economies, India’s general government debt is already among the lowest (alongside Germany) and is projected to fall from 81.3% of GDP in 2024 to 75.8% by 2030. Contrast that with the US, where debt is already above 120% and rising.

Capital Efficiency: India’s incremental capital-output ratio—a measure of how much investment is needed to generate growth—is far lower than in the US, China, Japan, or Germany. In plain terms, we get more economic bang for each rupee invested.

Balanced Trade Exposure: With exports at about 20% of GDP, we are less vulnerable to global trade shocks than export giants like Germany (where exports exceed 40% of GDP) but still integrated enough to benefit from global demand.

What It Means to Be Number Two

Crossing the threshold to become the world’s second-largest economy will reshape not just how others see us, but how we see ourselves.

- Geopolitical Clout: Economic size translates into influence—at the WTO, in climate negotiations, and in setting global technology standards.

- Investment Magnetism: Global capital chases growth. A bigger, faster-growing India will attract more foreign direct investment, fueling another cycle of expansion.

- Social Transformation: High growth, if made inclusive, can accelerate poverty reduction and expand the middle class, deepening domestic markets and political stability.

- Innovation at Scale: A vast home market enables the rapid scaling of innovations, from renewable energy to digital services, making India a global laboratory for solutions.

The Call to Action

Numbers and projections, however compelling, are not destiny. They are a map, not the journey. To make the 2038 milestone a reality, we will need to:

- Sustain Reform Momentum: Simplify regulations, reform labor laws, and ensure a stable tax regime to attract investment.

- Invest in Human Capital: Education and skill development must keep pace with technological change to ensure our young workforce is globally competitive.

- Build Resilient Infrastructure: From power grids to logistics, the backbone of a modern economy must be robust and future-ready.

- Guard Macroeconomic Stability: Prudent fiscal and monetary policies are essential to keeping inflation low, currency stable, and investor confidence high.

A Decade to Remember

In 1980, India’s economy was smaller than Brazil’s. In 2000, we were still an economic middleweight. By 2025, we are the world’s third-largest economy in PPP terms. And if EY’s projections hold, in just over a decade, we will overtake the United States itself.

This is not just a matter of national pride—it is a once-in-a-century opportunity. Managed well, it could secure prosperity for hundreds of millions, elevate India’s voice in shaping the global future, and prove that democracy and development can go hand in hand.

The rest of the world should take note: the next chapter of the global economy will not be written in Washington or Beijing alone. Increasingly, it will be drafted in New Delhi, Bengaluru, and Mumbai. And if we play our cards right, by 2038, India won’t just be part of the conversation—it will be leading it.